Copy Link

Copy Link Share on X

Share on X Share on Facebook

Share on Facebook Share on LinkedIn

Share on LinkedIn

Always Active

Required for core functionality such as security, network management, and accessibility. These cannot be disabled.

Build intelligent AI systems that automate decisions, accelerate innovation, and scale business growth.

Design, build, modernize, and scale digital products that drive business growth.

Build secure, scalable, and intelligent platforms that power modern enterprises.

Build intelligent, connected, and autonomous systems that operate in the real world.

Flexible engineering capacity with predictable delivery, ownership, and outcomes.

Uncover the transformative potential of digital and mobile solutions for your industry

Last Updated: Jul 15, 2026

Jun 18, 2026

Last Updated: Jul 15, 2026

Jun 18, 2026  239

239  28 min. Read

28 min. Read

Key Takeaways

The front door to every banking relationship is KYC. And for most firms right now, that front door is quietly doing serious damage – to conversion rates, to compliance team capacity, and to the customer experience before any actual banking has even happened.

According to Banking Dive, 25% of banking applications are abandoned due to KYC friction alone. The average KYC process costs between $1,500 and $3,500 per customer review, with some large institutional banks spending up to $35 million annually just to onboard 10,000 new clients. Fenergo’s 2025 Financial Crime Industry Trends report found that financial institutions spend an average of $72.9 million annually on KYC and AML operations combined – the majority of it on manual, repetitive work that is both slow and inconsistency-prone.

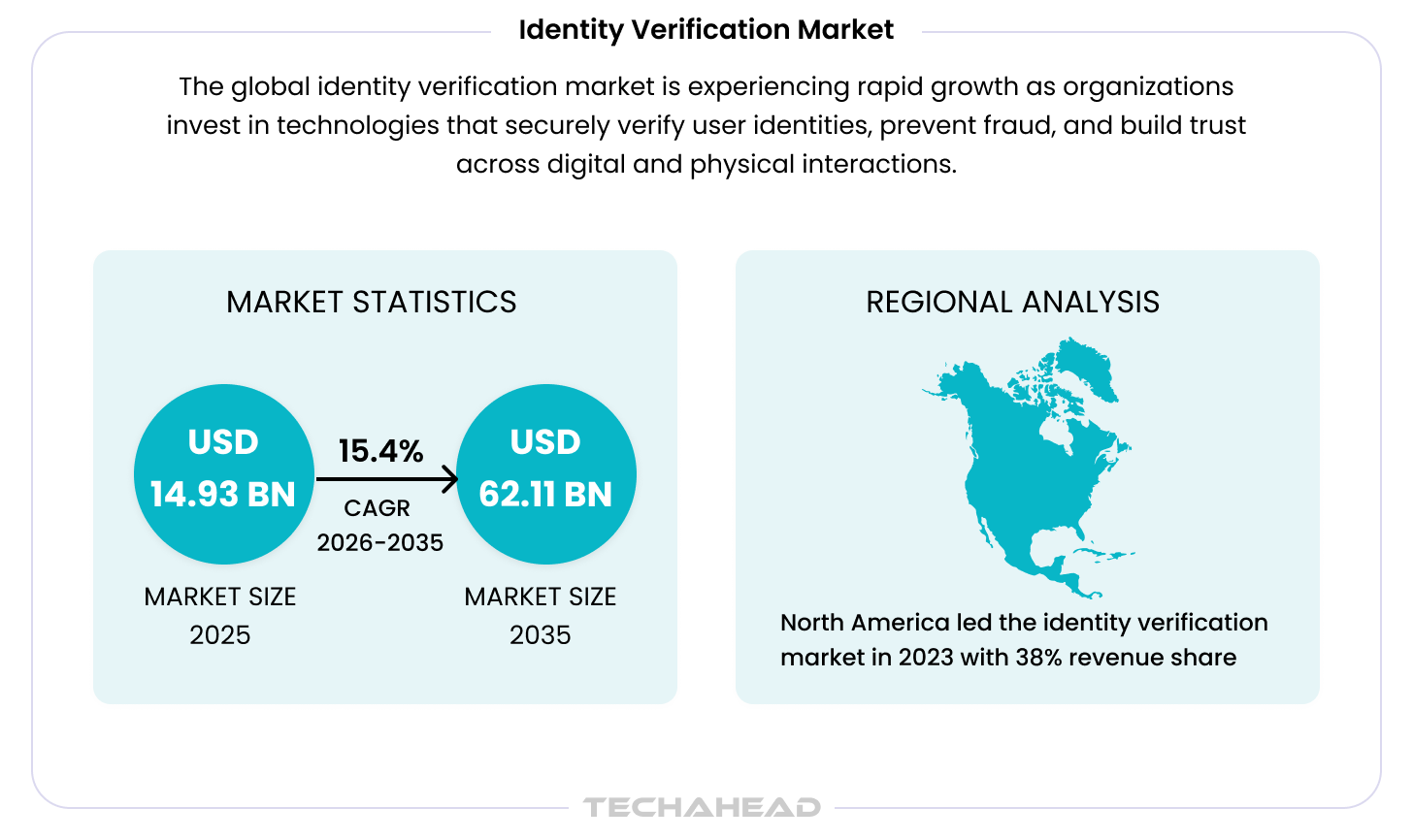

These numbers would be concerning enough in a stable market. But this is not a stable market. The global identity verification market was valued at $14.93 billion in 2025 and is projected to reach $62.11 billion by 2035, growing at a 15.4% CAGR, according to SNS Insider. The volume of customers to verify, the sophistication of identity fraud to detect, and the pace of regulatory change are all accelerating together.

Manual KYC was not designed for this environment. The institutions that recognize this early are not just solving an operational problem. They are building a structural competitive advantage.

AI agents for KYC systems are what that advantage looks like in practice – not a faster version of the old process, but a fundamentally different architecture. One that reasons through unstructured data, coordinates across systems simultaneously, and delivers consistent, auditable decisions at a speed that human reviewers working within manual workflows cannot match.

This blog covers what that looks like: the use cases, the architecture, and what it takes to build an AI-powered customer onboarding system – from eKYC for digital-native banks to full enterprise onboarding pipelines – that actually holds up under production conditions and regulatory examination.

Before getting into the solution, it is worth being clear about why legacy KYC fails the way it does – because the failure mode determines how you fix it.

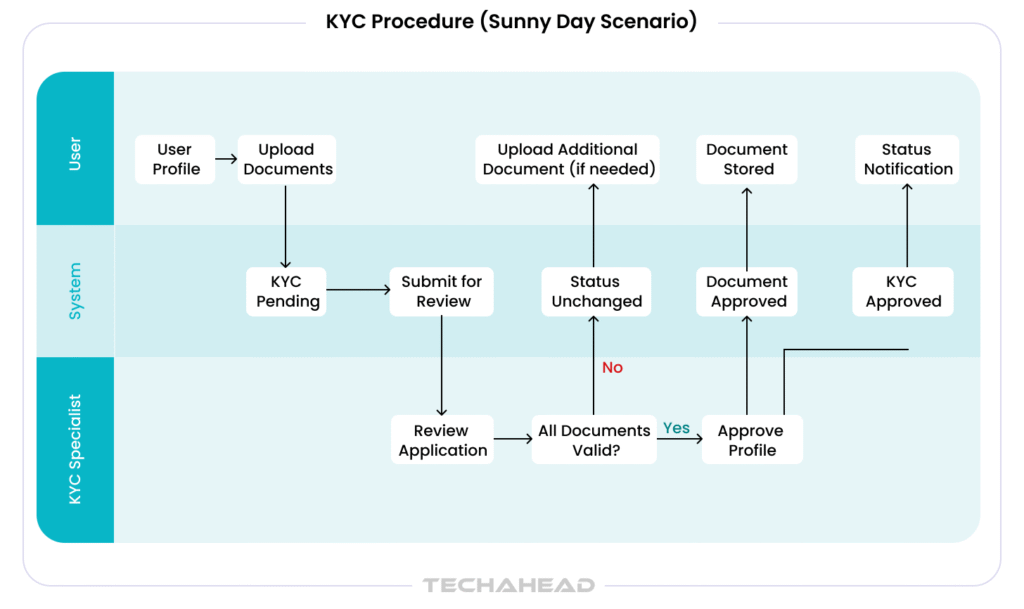

Manual KYC workflows are slow not because compliance teams lack diligence. They are slow because the process architecture was designed for a world of branch-based interactions, standardized document formats, and manageable transaction volumes. That world no longer exists.

What legacy KYC processes produce instead:

The compliance exposure compounds the operational drag. 90% of surveyed banks report that human error directly impacts risk decision-making quality. And when errors surface during regulatory examination – months after the original decision – the remediation cost dwarfs whatever efficiency saving the manual process was supposed to deliver.

TD Bank’s $3 billion penalty in 2024 – the largest in US banking history for Bank Secrecy Act and AML compliance failures, including systemic KYC breakdowns – is the number that turns that abstract risk into a board-level conversation. The question for every institution still running manual KYC workflows is not whether that kind of exposure exists. It is how long the current architecture stays defensible before an examiner finds the gap first.

This is the architecture problem that AI agents for KYC systems solve. Not automation layered over a broken process, but a rebuilt decision pipeline where specialized agents reason, coordinate, and escalate correctly from the very first interaction. Continuous monitoring and transaction monitoring are integral to this approach, ensuring emerging threats and compliance risks are detected promptly.

Related: Multi Agent Architecture Guide for AI Dispute Resolution

If your institution has already deployed RPA in back-office compliance workflows, the obvious question is: what does an AI agent do that existing automation does not?

The honest answer is that they solve a fundamentally different problem.

RPA is an execution tool. It handles predictable, structured inputs – copying data between systems, triggering actions based on fixed rules, processing documents that always look the same. When a document format changes, when a data field is missing, or when a case falls outside the defined rule set, RPA fails or escalates to a human. It cannot reason through ambiguity.

AI agents for KYC operate at a different level entirely. They interpret unstructured identity documents, reason through incomplete data, identify anomalies that deviate from behavioral norms, and coordinate across multiple systems simultaneously – adapting to the edge cases that break rule-based automation while maintaining an auditable reasoning trail, not just an activity log. They use advanced behavioral analytics and financial crime compliance techniques to detect identity theft and other potential risks. Leveraging large language models, these agents enhance risk management by continuously updating risk profiles and conducting adverse media screening.

Related: Types of LLMs Powering Modern AI Agents in 2026

For KYC automation banking, this distinction is not academic. Customer documents vary. Sanctions databases update in real time. Risk profiles need rebuilding when customer circumstances change. These are precisely the conditions where rule-based automation hits its ceiling and where domain-trained AI agents take over as the intelligent processing layer.

RPA and AI agents are not competitors – they are complementary. Predictable, rules-based steps in onboarding workflows can stay on RPA. The judgment-heavy parts – document interpretation, anomaly detection, real-time risk scoring, and semantic search – belong to AI agents. Getting that boundary right is where good architecture starts.

For a broader view of where vertical AI agents in fintech sit across KYC, AML, fraud detection, and dispute resolution, the pillar blog covers all six fintech functions in full.

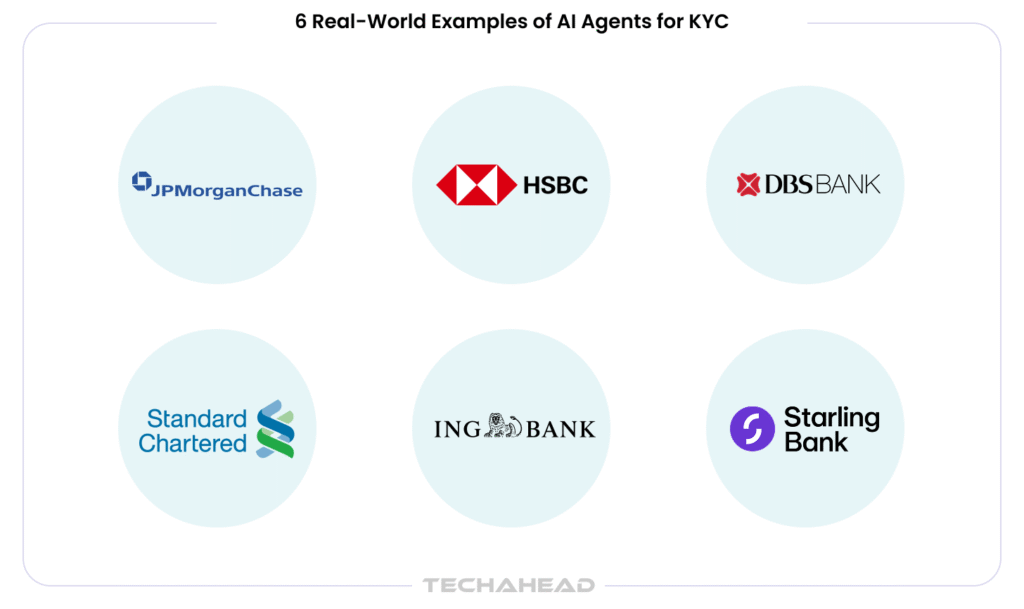

These are not pilot programs or proof of concepts. These are institutions that have moved from evaluation to production – and what they built is instructive.

JPMorgan Chase is deploying a new agentic AI-based KYC onboarding system, reported by Risk.net to be targeted for production by the end of April 2026. A process that previously took up to five days is being compressed to under one minute. The bank’s framing is explicitly “agentic-first” – meaning agents orchestrate the entire onboarding workflow from intake, rather than being embedded as acceleration layers within existing sequential processes.

The takeaway for your institution: JPMorgan is not automating their old process. They are replacing the process architecture entirely. That decision – full workflow reimagination rather than incremental tooling is the architectural pattern responsible for the time compression result.

In its Q4 2025 earnings call, HSBC detailed an accelerated AI-led transformation spanning onboarding, KYC, fraud detection, credit applications, and contact center automation, with $1.8 billion reallocated toward digital banking priorities. The bank appointed its first Chief AI Officer and is treating AI-powered customer onboarding not as an isolated compliance function but as a connected layer across the entire customer lifecycle.

The takeaway for your institution: HSBC’s approach reflects a shared data architecture across onboarding, KYC, and AML, so each function benefits from intelligence gathered at every other touchpoint. The operational and compliance gains compound because the data infrastructure is unified, not siloed.

ING Bank is rebuilding its KYC workflows using agentic AI with a specific design principle: reduce what clients are required to provide by drawing on data ING already has access to from public registries and existing behavioral data. “All the manual work we do in client due diligence, KYC, will largely be redone with a new model based on existing/available data, so we do not have to ask clients for all the data points,” said ING’s Head of Data and Analytics. Agentic AI-generated mortgage workflows were planned to follow in 2026.

The takeaway for your institution: ING’s approach demonstrates a key principle of good automated KYC onboarding – the agent should minimize client burden, not just analyst burden. Pulling simultaneously from public registries, behavioral data, and existing CRM records is what makes this possible.

DBS Bank Hong Kong partnered with Know Your Customer Limited in March 2026 to automate SME onboarding workflows. The system provides real-time access to official company documents and automatically identifies complex Ultimate Beneficial Ownership (UBO) networks across more than 140 jurisdictions – a process that was previously manual, cumbersome, and a significant source of onboarding delays for business customers.

The takeaway for your institution: Corporate KYC is structurally more complex than consumer KYC. UBO mapping across jurisdictions, corporate document verification, and entity relationship analysis require the parallel processing capability that only multi-agent AI systems can deliver at production scale.

Standard Chartered is one of the institutions reported by Risk.net to be actively planning agentic AI deployment specifically for KYC onboarding workflows, named alongside JPMorgan and ING in the same industry disclosure. The bank’s inclusion in this group signals that agentic-first KYC reimagination is moving from a single-institution bet to a coordinated shift across major global banks at the same time.

The takeaway for your institution: When three global banks disclose the same architectural direction within the same reporting cycle, that is not a coincidence. It is a signal that the agentic-first approach to KYC has cleared internal risk and governance review at multiple large institutions simultaneously, which matters if your own governance team is still asking whether this is proven enough to commit to.

Starling Bank uses AI-driven facial recognition verification as a core component of its digital account opening process, validating identity in real time while maintaining AI KYC compliance standards. This is a single-model verification capability rather than a multi-agent system, but it is a clear example of production-grade AI delivering both speed and compliance at the exact moment a customer relationship begins. The result is faster onboarding with materially lower abandonment and stronger fraud prevention than document-only approaches.

The takeaway for your institution: Not every high-impact AI deployment in KYC needs to be a full multi-agent system from day one. Starling shows that even a single well-built AI capability, deployed at the right point in the onboarding journey, delivers a measurable customer experience and fraud prevention dividend.

These six institutions operate at different scales, serve different customer segments, and sit at different stages of AI maturity – from JPMorgan and ING’s full agentic rebuilds, to Standard Chartered’s disclosed plans, to Starling’s targeted use of AI at a single critical step.

What they share is a strategic conclusion, not an identical implementation: sequential, manual KYC workflows are the constraint worth solving for, and AI, deployed at the right depth for your institution’s complexity, is how you solve it. That conclusion is not reserved for tier-one banks with nine-figure technology budgets. The same architectural principles JPMorgan is applying at enterprise scale work equally well for a 200,000-customer digital bank building its first KYC pipeline or a regional lender replacing a compliance workflow that has not been modernized in a decade. The depth of the build should match your complexity. The business case holds at every size.

“The institutions that get AI agents for KYC right are not the ones that automated their existing workflow. They are the ones that asked what the workflow should look like if you designed it from scratch with AI at the center – and then built exactly that. That is the question we start with at TechAhead on every financial services onboarding”

— Vikas Kaushik, CEO, TechAhead

Understanding the use cases is one thing. Understanding the build is where most initiatives stall – and where most decisions that determine production success or failure get made. Here is what a production-grade multi-agent KYC system looks like from an architecture perspective.

Also Read: Agentic AI Development Guide

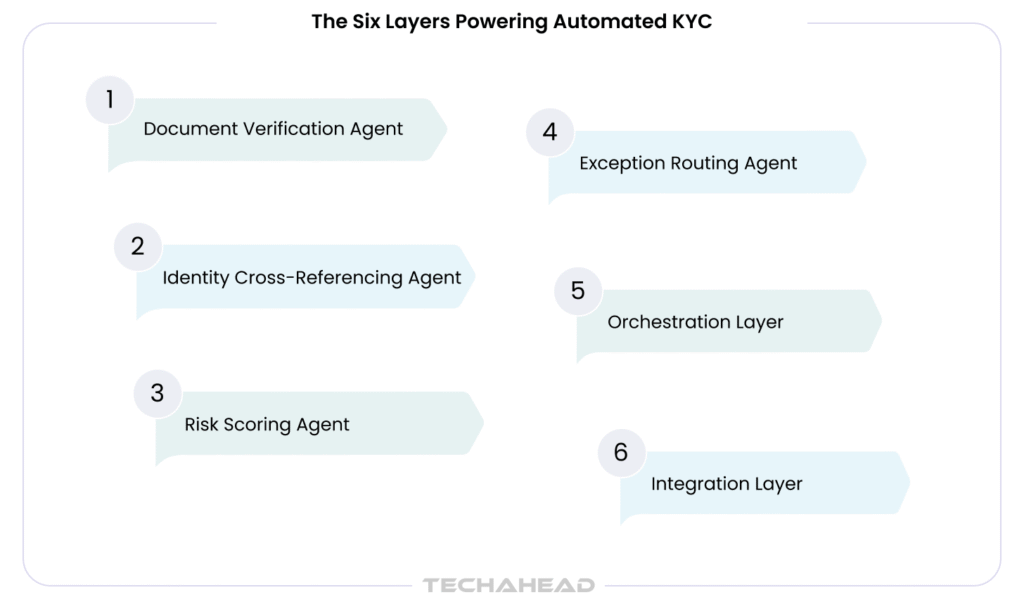

The core insight: no single agent should own the entire KYC workflow. A single generalized agent trying to handle document verification, sanctions screening, risk scoring, and exception routing simultaneously becomes unreliable across all four functions. The architecture that works deploys specialized agents for each domain, coordinated by an orchestration layer.

Handles document ingestion before it reads and authenticates identity documents – passports, national IDs, utility bills, corporate registration certificates – using optical character recognition to extract data from passports, IDs, and corporate documents against issuer databases and behavioral signals in real time. Detects tampering, expiration, and cross-field inconsistencies. OCR-based extraction across multiple document formats helps improve accuracy in downstream checks. In 2026, this function also includes deepfake detection, which is an increasingly common attack vector in digital onboarding pipelines. Intelligent document processing at this layer is where the quality of the entire downstream workflow is determined.

Checks identity data simultaneously against global sanctions lists, PEP (Politically Exposed Person) databases, and adverse media sources. The “simultaneously” is the important word. Sequential screening adds hours. Parallel agent processing compresses it to seconds. This is where automated identity verification delivers its most visible time savings for compliance teams.

Generates real-time customer risk scores across different customer scenarios by analyzing financial behavior, geographic signals, document verification outputs, screening results, and other risk indicators. The risk score is not a black-box output – it is a documented, auditable reasoning chain that compliance officers can interrogate when a specific decision is questioned later. Well-designed AI risk engines can enhance detection accuracy by 30% in KYC processes. This auditability requirement shapes how this agent is built from the start.

Handles cases that exceed defined risk thresholds, contain unresolvable ambiguity, or show low confidence scores. These cases are escalated to human review – but not as raw data. The exception routing agent pre-assembles a complete case file with all relevant evidence, so reviewing analysts make judgment calls rather than spending time reconstructing context from scattered system records. This cuts manual intervention and can reduce manual review workload by 85% by sending analysts only the ambiguous cases.

The coordination mechanism that ties all four agents together. It manages handoffs, maintains workflow state across steps, supports case management for downstream investigation handling, handles failure modes without silently dropping decisions, and maintains the complete sequence of operations required for a regulatory-grade audit trail. When orchestration is tied to case management, AI-driven tools can reduce compliance reporting times by 25%. The orchestration layer is also where human-in-the-loop triggers are defined – the precise conditions under which a case moves from autonomous processing to analyst review.

For a deeper look at how the agent loop operates in production multi-agent systems – how agents reason, plan, and hand off across steps – the concepts map directly to KYC architectures.

A KYC agent system does not operate in isolation. It needs to connect to core banking systems, CRM platforms, legacy systems, AI AML monitoring stacks, and downstream data pipelines. This layer handles banking-grade API security, data validation before system writes are committed, and the integration patterns that allow the AI compliance layer to coexist with existing infrastructure – not requiring a full platform replacement. Even so, integrating AI agents with older environments can still be complex.

Must Read: 7 Ways Multi-Agent AI Fails in Production

TechAhead has architected AI-powered compliance workflows for enterprise financial services clients, building audit-ready document processing and identity verification pipelines that handle high-volume sensitive data under strict governance standards. The architecture patterns developed in these engagements transfer directly to production KYC builds.

Consumer KYC handles individual identity. Know Your Business (KYB) – the corporate onboarding equivalent – is structurally more complex, and for most commercial banks and lending platforms, an even bigger source of operational drag.

KYB requires verifying corporate structures, identifying Ultimate Beneficial Owners (UBOs) across potentially multi-layered ownership hierarchies, cross-checking against corporate registries across jurisdictions, assessing counterparty risk, and maintaining ongoing monitoring as corporate structures change over time. Doing this manually for a mid-market corporate client routinely takes weeks.

AI agents for KYB apply the same multi-agent architecture principles with domain-specific additions:

The DBS Bank Hong Kong example from earlier – automating UBO identification across 140 jurisdictions – is a direct demonstration of what production KYB agent architecture delivers. What was previously a multi-day manual research workflow becomes a real-time automated check with a documented, retrievable output.

For banks with significant commercial banking, SME lending, or fintech partnership operations, adding KYB capability to the same agent infrastructure as consumer KYC creates a shared AI KYC compliance layer rather than two separate systems with separate data pipelines and separate governance frameworks.

TechAhead builds AI development systems, not compliance programs. But in financial services, the two are architecturally inseparable – and the mistake most AI implementations make is treating compliance requirements and enterprise regulatory compliance as something you add near the end of the build.

The correct framing: KYC regulatory requirements – FATF Recommendations 10 and 12, FinCEN’s Customer Identification Program (CIP) rules under the BSA, and the EU’s successive Anti-Money Laundering Directives – are not constraints on what an AI agent can do. They are specifications that define what the agent must be able to prove about every decision it makes. In the financial industry, traditional know your customer KYC methods and periodic reviews were built for a less digital environment.

Also Read: EU AI Compliance Checklist for Software Vendors

That framing changes the architecture in three specific ways:

The cost of getting this wrong is not hypothetical. TD Bank’s $3 billion BSA and AML penalty in 2024 included specific findings around KYC process failures – inadequate customer risk profiling, incomplete monitoring, and documentation gaps that examiners traced directly back to how the underlying systems were built. The penalty was not the result of bad intent. It was the result of an architecture that could not produce what regulators needed to see. Building compliance into the system from day one is not the cautious approach. It is the only approach that does not leave your institution exposed to the same finding.

For more on how SOC 2 controls apply specifically to AI systems in financial services – including audit trail requirements and evidence collection standards – the linked blog covers the specifics in depth.

“Every KYC AI engagement at TechAhead starts with one architecture question: what does a regulator need to see about this decision, and can the system produce it on demand? Building the audit infrastructure before the agents are designed changes the entire approach to the build. It is also, frankly, what separates systems that reach production from systems that don’t.”

— Deepak Sinha, CTO, TechAhead

The business case for AI agents in KYC systems rests on measurable outcomes and compliance efficiency, not capability descriptions. Here is what institutions that have moved from pilot to production are reporting:

| Metric | Manual Baseline | AI Agent Benchmark |

| Standard-risk onboarding time | 3–7 days | Under 5 minutes |

| Cost per customer review | USD 1,500–3,500 | Significantly reduced at scale |

| KYC/AML review time | Baseline process | Up to 60% faster |

| False positives in screening | High; requires manual assessment | Up to 60% fewer |

| Application abandonment due to KYC friction | ~25% of applicants | Materially reduced |

| Banks reporting human-error impacts on risk decisions | ~90% | Reduced through consistent agent-driven decision logic |

Top deployments report compliance efficiency improvements of 200 to 2,000 percent. AI reduces KYC processing time by 90% when banks redesign the workflow around coordinated agents rather than layering AI onto manual steps. These figures reflect institutions deploying production-grade agentic AI onboarding systems – not averages from controlled pilots. The spread in outcomes tracks with architecture decisions: banks that rebuilt the KYC workflow around agent coordination see the higher end of these ranges. Those that added AI layers on top of existing sequential processes see incremental improvement, not just mere transformation.

One additional data point worth noting: 82% of financial institutions are already using AI to automate labor-intensive KYC and AML processes. The question for the remaining 18% is no longer whether to adopt – it is how to build so that what they deploy actually holds up in production and under examination.

The gains from well-built AI-powered CDD banking systems also compound over time. The institutions reporting the strongest results in 2026 are the ones that started building in 2024 and 2025 – because every quarter of production data makes their agents more accurate and their models more defensible.

When TechAhead worked with American Express on their fraud detection AI infrastructure, the focus was structured incident classification and tighter model governance – reducing AmEx’s false positive rate by 28% through more precise alerting and escalation architecture. The same governance discipline applied to AI agents for KYC systems is what makes their outputs defensible under examination.

Off-the-shelf KYC platforms will tell you they can do most of this. And for a small institution with a straightforward onboarding workflow and no legacy infrastructure to contend with, that might even be true; in the financial industry’s larger firms, however, integration demands and operational costs make packaged tools far less attractive. But most financial institutions reading this are not that institution.

The ceiling on pre-built platforms tends to show up in the same three places every time:

Buying a platform is faster to deploy. It is also a permanent trade of depth for speed. For institutions where KYC directly affects how fast you acquire customers and how exposed you are when compliance gaps surface, that trade tends to age poorly. Custom AI solutions are often justified when the upside includes lower overhead and the potential to save financial institutions $60M–$500M annually at scale.

TechAhead is an AI development and consulting company. We build production-grade automated KYC onboarding systems for financial services institutions – not compliance programs, but the technology infrastructure that compliance operations run on.

What that looks like in practice:

Our credential stack matters in this context specifically. ISO 42001:2023 governs how every Agentic AI system TechAhead develops is designed, documented, and maintained. SOC 2 Type II means data security controls across every engagement are continuously audited by an independent third party – a relevant distinction when the data being processed is customer PII, identity documents, and financial records. As an AWS Advanced Tier Partner with Security Services Competency and Claude + OpenAI Services Partner, the infrastructure and model access available inside every TechAhead engagement meet the standards that financial services procurement teams mandate.

Clients including AXA and American Express represent the tier of regulated financial services environment our AI systems operate within. The delivery standard that makes those engagements work is the same standard applied to every AI-powered CDD banking build we take on.

If your institution is evaluating an AI KYC implementation partner – whether you’re a digital bank building your first onboarding architecture or a traditional bank replacing a decade-old compliance workflow, TechAhead’s enterprise delivery team can assess your requirements and map the path from current state to production. Contact TechAhead to start that conversation.

Yes, and the numbers are not theoretical. AI agents for KYC systems running in production compress standard-risk onboarding from three to seven days to under five minutes. JPMorgan’s deployment goes further – a five-day process reduced to under one minute.

AI document verification agents use generative AI to extract and review identity data against issuer databases in real time, while still checking for tampering, expired fields, and deepfake submissions simultaneously. Unlike manual review, accuracy does not degrade with volume or reviewer fatigue, which is the part most institutions underestimate. In well-governed workflows, this can reduce KYC processing time by 90%. When paired with verification controls, it can improve KYC accuracy to 99.5%.

Built correctly, yes. A well-architected AI KYC compliance system aligns with FATF Recommendations 10 and 12, FinCEN CIP rules, and EU AML Directives. The key is treating regulatory requirements as architecture specifications from the start, not compliance boxes to check at product close.

Every agent decision needs to be timestamped, logged, and retrievable as a documented reasoning chain. “The model said so” is not a defensible answer to an examiner. Regulators want to see what evidence was considered and how every outcome was reached.

Depends on your complexity. Off-the-shelf platforms hit a ceiling fast on integration depth and configurability. A custom multi-agent KYC system is built around your infrastructure and risk thresholds, and critically, the audit trail lives in your environment, not a vendor’s server. Security considerations matter here, especially for agentic AI systems and AI models where contextual accuracy can break down in regulated workflows.

It is triggered at defined risk thresholds, not across every case. Standard-risk applications process autonomously end to end. High-risk or ambiguous cases escalate to analysts with a pre-assembled evidence file. The goal is redirecting human judgment to where it actually matters. In supervised agent workflows, it can enhance risk profiling accuracy by 30%.

Yes, though KYB is structurally more complex. AI agents for KYB map corporate ownership hierarchies, identify UBOs across jurisdictions, and run entity-level sanctions screening in parallel. The same multi-agent AI infrastructure handles both on a shared compliance and data layer.

Start with ISO 42001:2023 AI governance certification, SOC 2 Type II, and verifiable experience in regulated financial services. Beyond credentials, a serious AI KYC implementation partner starts with workflow mapping and compliance architecture, not a product demo and an immediate statement of work.

We use cookies to ensure our website functions properly, improve performance, and provide a personalized experience. You can choose which types of cookies to allow below.

Required for core functionality such as security, network management, and accessibility. These cannot be disabled.

Help us understand site traffic and user interactions so we can improve performance and usability.

Enable enhanced functionality and personalization such as language or region preferences.

Used to deliver relevant ads, track campaign performance, and measure advertising effectiveness.