Copy Link

Copy Link Share on X

Share on X Share on Facebook

Share on Facebook Share on LinkedIn

Share on LinkedIn

Always Active

Required for core functionality such as security, network management, and accessibility. These cannot be disabled.

Build intelligent AI systems that automate decisions, accelerate innovation, and scale business growth.

Design, build, modernize, and scale digital products that drive business growth.

Build secure, scalable, and intelligent platforms that power modern enterprises.

Build intelligent, connected, and autonomous systems that operate in the real world.

Flexible engineering capacity with predictable delivery, ownership, and outcomes.

Uncover the transformative potential of digital and mobile solutions for your industry

Last Updated: Aug 4, 2026

Jun 5, 2026

Last Updated: Aug 4, 2026

Jun 5, 2026  396

396  46 min. Read

46 min. Read

Key Takeaways

Let’s evaluate your readiness and calculate your score in minutes

Fintech does not reward the institutions that understood AI agents first. It rewards the ones that built correctly and deployed fastest. The understanding part is largely done across the industry. What is separating fintech firms right now is the quality of what they built, and whether it is actually running in production or sitting in a slide deck from last year’s strategy offsite.

That gap is not a technology gap. It is a build gap.

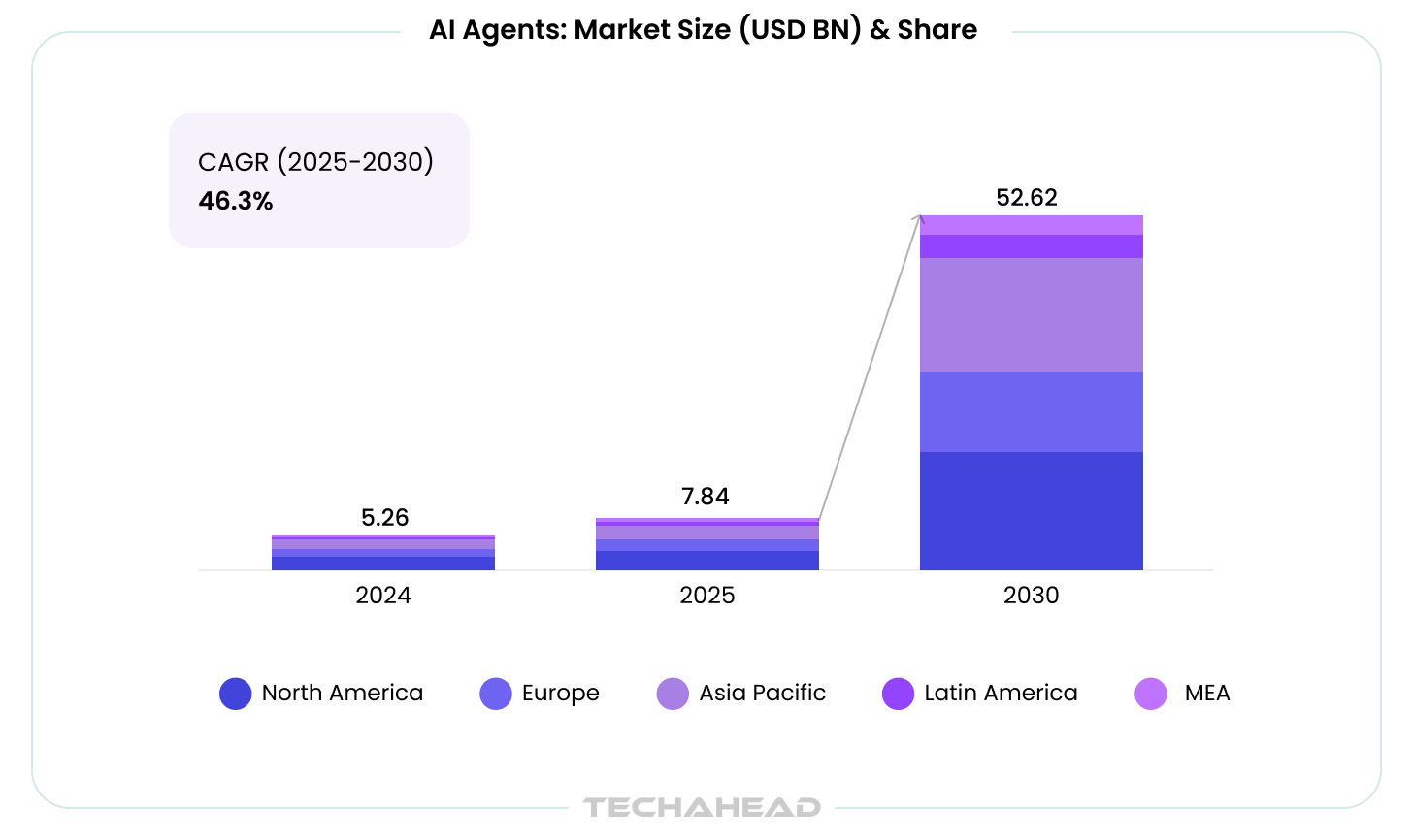

The numbers behind it make the urgency impossible to ignore. According to Wolters Kluwer, 44% of finance teams are using agentic AI in 2026, a figure representing a 600% jump from 2025. The global AI agents market is moving from $7.84 billion in 2025 to $52.62 billion by 2030, compounding at a 46.3% CAGR. The returns are real, but they are not automatic. Every organization that has captured them did so by building correctly, not by deploying quickly.

The firms capturing that return share one thing in common: they stopped running pilots and started building production-grade systems, with engineering discipline, regulatory awareness, and the right development partner. The firms still waiting are not protecting themselves from risk. They are accumulating it.

This is not a blog about why AI is transforming fintech. You already know that. This is a builder’s guide for executives who are past the awareness stage and into the execution stage. Business owners who need to make real architectural decisions. Executives who need to understand what a credible fintech AI development investment actually looks like. Senior leaders who have learned, through observation or hard experience, that generic AI deployed in a regulated financial environment is not the same thing as a vertical AI agent purpose-built for it.

We will cover the six fintech functions where AI agents in fintech are generating the most measurable, production-grade results right now.

By the end of this, you will have a clear picture of what good looks like, and what your next step should be.

Here is a distinction that sounds subtle but carries material consequences for every fintech AI you will ever consider: a vertical AI agent is not a general-purpose AI model with a system prompt that says “you are a compliance assistant.” It is an AI system purpose-built for a specific domain, trained on domain-specific data, aware of domain-specific regulatory requirements, and capable of domain-specific reasoning at production scale, with a full audit trail.

In most industries, the difference between a horizontal and a vertical AI approach is a performance trade-off. In financial services, it is a regulatory and reputational one.

Must Read: Expanding Digital Natives to Transform Industries

Generic AI – the horizontal models most financial institutions have experimented with – fails in fintech for three specific, structural reasons:

The result of deploying the wrong tool is not just underperformance. It is compliance exposure at scale. Rule-based or generic AI systems making high-volume decisions in regulated financial workflows without proper auditability trails are a liability that compounds quietly until a regulatory examination surfaces it.

“In fintech, the margin for error is not a setting you configure but is the environment you build for. Every AI agent we deploy at TechAhead starts with one foundational question: can this decision be explained, defended, and audited when a regulator asks? That is not a constraint on what AI can do. It is the foundation that makes it trustworthy enough to do it at scale.”

— Vikas Kaushik, CEO, TechAhead

The shift from horizontal to vertical AI agents in fintech is a structural correction happening across the industry right now. Enterprises that deployed generic AI in financial workflows and then wondered why adoption stalled or why compliance teams pushed back – were solving the right problem with the wrong architecture.

At TechAhead, every fintech AI development begins with the domain specificity question: what does this agent need to know, what decisions does it need to make, and what does it need to prove?

Getting those three questions right before a single line of code is written is the difference between an AI agent that reaches production and one that does not.

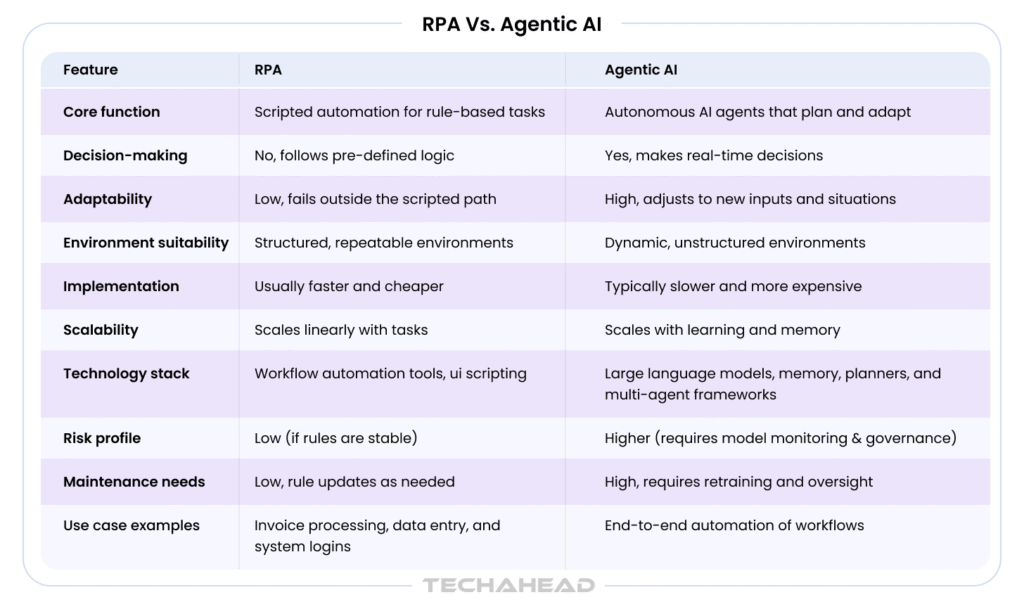

If your institution already has RPA deployed across back-office workflows, the first question your technology team will ask about AI agents is a fair one: what does this do that our existing automation does not?

The honest answer is that, unlike traditional automation tools, RPA and AI agents are not competing tools. They solve fundamentally different problems. Knowing which problem you have is what determines which solution you need.

Related: How RPA can Transform Businesses

RPA operates on rules and structure. Unlike traditional automation tools, AI agents can interpret context and adapt, while RPA executes predefined workflows across predictable inputs – copying data between systems, triggering actions based on fixed conditions, processing documents that always look the same. It does not reason. It does not handle exceptions. And when something falls outside the defined workflow, it fails or escalates to a human.

Vertical AI agents operate differently at a foundational level:

In fintech specifically, the limitation of RPA surfaces fastest in compliance-heavy workflows. AML typologies evolve. Customer documents vary. Dispute narratives are unstructured. These are exactly the environments where rule-based automation hits its ceiling and domain-trained AI agents take over as autonomous software systems with minimal human oversight.

TechAhead works with institutions that have both RPA and AI agent infrastructure. The question is never either/or. It is knowing precisely where each belongs in your operational stack.

Every major financial institution has an AI agent strategy. Considerably fewer have an AI agent in production. That distance between strategy and deployment is where most of the industry is currently stuck, and it is not a funding problem.

Must Read: Building Blocks of Successful AI Agents

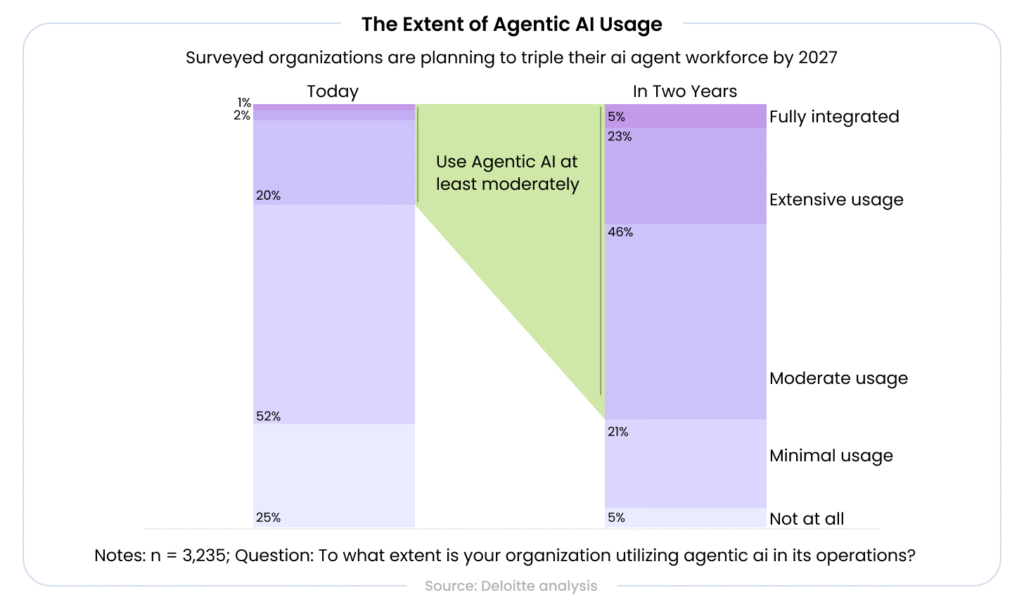

Here is where the conversation gets uncomfortable. Gartner projects that more than 40% of agentic AI projects will be cancelled by end of 2027, primarily due to escalating costs, unclear business value, and inadequate risk controls. And Deloitte’s 2026 State of AI in the Enterprise report, drawing on responses from 3,235 business and IT leaders across 24 countries, shows that only 21% of companies have a mature governance model in place for their AI agents. The majority of enterprises are either running agents without adequate oversight or stalling at the pilot stage precisely because they cannot establish it.

This is not a technology problem. The technology works. What does not work is deploying it without the engineering discipline, regulatory expertise, and production-grade architecture that a regulated financial environment demands.

Recommended: Enterprise AI Scaling

The firms whose AI agents are delivering ROI did not simply buy the best model. What they did differently:

TechAhead’s approach to AI agents for financial services is built around this reality. The gap between a fintech AI agent that delivers measurable ROI and one that gets cancelled in a board review is engineering discipline and build quality, not ambition.

The six functions below represent the highest-impact areas where AI agents in fintech are moving from pilot programs into production across banks, digital lenders, payment platforms, and financial services firms. Each one is a distinct operational challenge. Each one is also a connected piece of a larger AI architecture, and the firms building them as a connected system rather than isolated deployments are the ones compounding the advantage.

Here is what each function looks like when it is built correctly.

Every customer relationship in financial services begins at the same place: onboarding. And for most banks and fintechs, that starting point is where the most friction lives and where the most compliance risk concentrates simultaneously.

The economics of manual KYC are simply not sustainable at scale. Manual verification processes carry average completion times of several days, with customer drop-off rates that compound at every delay point. For institutions processing high volumes (challenger banks, digital lenders, payment platforms), the cost per manually verified customer runs into hundreds of dollars once analyst hours, error correction cycles, and re-verification work are fully accounted for.

Automating routine tasks in onboarding removes delays around routine tasks and helps reduce operational costs. But the real cost is not the operating expense. Human reviewers apply standards inconsistently across cases. Documentation gaps surface during regulatory audits months after the original interaction. And customers who experience friction at onboarding do not complain – they leave.

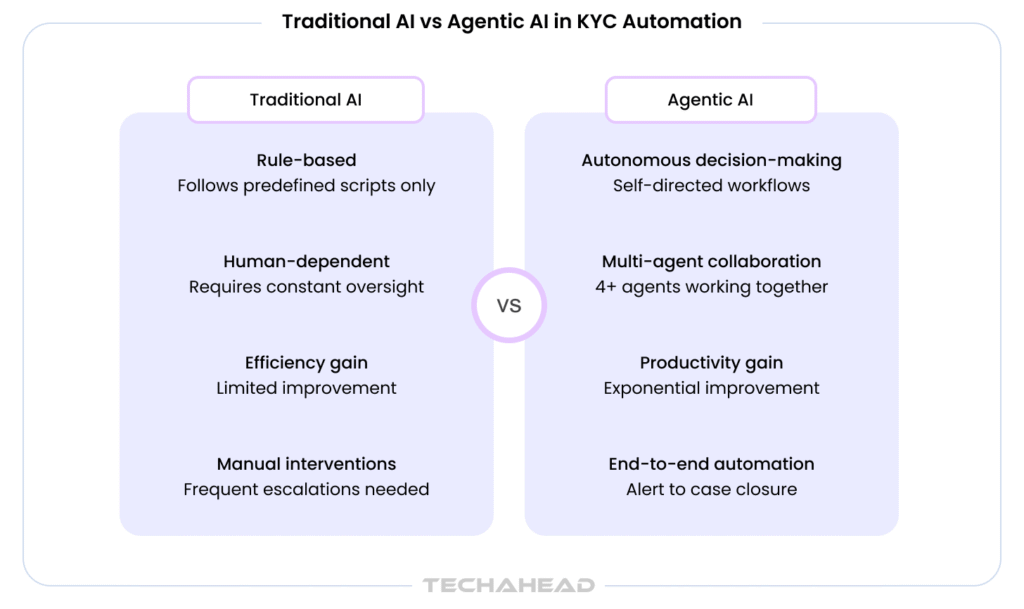

AI agents for KYC and customer onboarding in banking address this at a structural level. A well-architected KYC agent workflow is not a single agent doing everything. It is a coordinated system of specialized agents, each expert in its function:

The regulatory layer is not an add-on to this workflow. It is the workflow. FATF recommendations, regional AML directives, and jurisdiction-specific identity verification requirements are embedded in the agent’s decision logic from architecture stage onward. This is what separates building a custom AI agent for financial services from a generic automation script: the regulatory framework is not consulted after the decision, it shapes the decision at every step across financial processes.

The customer experience impact is material and measurable. Fintech firms that have deployed AI-powered KYC agents report standard-risk onboarding completion times dropping from days to minutes, while high-risk cases receive more thorough, better-documented human attention because the agent has pre-processed the evidence and surfaced the specific concerns that need human judgment. Similar underwriting workflows show AI agents can approve over 80% of loans instantly once onboarding and verification data are structured correctly.

Faster onboarding is not just an operational win. In a competitive market where challenger banks are onboarding customers in under five minutes, speed is a conversion metric. Every day of delay in a manual KYC process is a percentage point of customer drop-off that your marketing budget cannot recover.

Recommended: Impact of Tokenized Securities on the Financial Industry

At TechAhead, AI agents for KYC and customer onboarding are built around three non-negotiable pillars: speed that reaches the customer experience layer, compliance that stands up to regulatory examination, and scalability that does not degrade as transaction volumes grow. These are not aspirational outcomes but are architecture requirements defined in week one of every engagement.

Once a customer is onboarded, the compliance work does not stop. For AML teams, it is only beginning – and for most of them, it is a crisis that compounds daily. Connected anti money laundering responsibilities now span compliance monitoring, regulatory reporting, and financial reporting, so gaps in one workflow quickly create pressure across the others.

The false positive problem in AML monitoring is one of the most persistent and expensive operational failures in financial services. Legacy rule-based AML systems generate alert volumes that compliance teams physically cannot process at adequate quality. Industry research consistently shows that between 90% and 95% of AML alerts generated by rule-based systems are false positives. For a mid-sized bank processing millions of transactions, that translates to thousands of analyst hours spent investigating alerts that lead nowhere, while genuinely suspicious activity may be moving through in patterns the rules were not written to catch.

AI-powered AML agents approach this problem at a structural level that rule-based systems fundamentally cannot:

Intelligent document processing can also automate regulatory filings and compliance checks tied to AML casework.

Related: Top AI Security Risks & How to Prevent Them

What most discussions of AML AI miss entirely is the audit trail requirement. This is not a compliance checkbox. It is an architecture constraint that fundamentally shapes how the agent reasons and how the system is built. Every decision the AML agent makes – every flag it raises, every case it deprioritizes, every typology pattern it identifies, must be explainable and retrievable when a FinCEN examiner or a BSA compliance officer asks about it months later. This requirement cannot be added to an AML agent after the build. It has to be in the design from the first architecture session. 53% of executives worry about regulatory compliance constraints, which is why explainable AML workflows matter.

TechAhead builds AI agents for AML compliance in banking with this constraint as a first principle. The AML agents we deploy are not just accurate. They are regulator-explainable, operationally efficient for the compliance teams who live in them daily, and built to adapt as both AML typologies and BSA regulatory expectations evolve over time. Over 80% of fintech firms leverage AI for fraud detection and adjacent monitoring functions, and production AML agents can significantly reduce fraud response time when alerts are prioritized correctly.

3. AI-Powered Fraud Detection: From Reactive Flagging to Real-Time Prevention

Fraud in financial services is no longer a problem of detection. It is a problem of speed. By the time a legacy fraud detection system flags a suspicious transaction, the transaction has already been processed. The customer has already been impacted. And the institution is already absorbing the loss.

The shift that AI agents for fraud detection in fintech enable is not just faster flagging.

It is a fundamental move from reactive to predictive:

From systems that identify fraud after the fact to agents that assess fraud probability in real time, at the transaction level, before authorization is granted, protecting financial transactions through stronger security and risk management.

Legacy fraud detection systems share the same structural weakness as rule-based AML systems: fixed thresholds applied to individual transactions in isolation. They do not see across accounts. They do not see across time. And they do not adapt to the fraud patterns that evolve specifically to evade them. The result is a familiar combination of high false positive rates that frustrate legitimate customers and genuine fraud slipping through in patterns the rules were not designed to catch.

What a production-grade fraud detection AI agent looks like in practice:

The customer experience dimension matters here as much as the security dimension. False positives in fraud detection do not just waste analyst time. They block legitimate transactions, frustrate customers at the point of payment, and generate complaints and disputes downstream. A well-built fraud detection agent reduces both fraud losses and false positive rates simultaneously because accuracy at the transaction level serves both outcomes.

Over 80% of fintech firms use AI for fraud detection. AI systems can introduce new cybersecurity vulnerabilities and data breaches, so fraud systems must be designed to avoid data privacy violations that can lead to significant financial penalties.

At TechAhead, AI-powered fraud detection systems are built with real-time inference speed, behavioral intelligence, and regulatory auditability as simultaneous requirements. The fraud detection layer we engineer does not operate in isolation, it shares data infrastructure with AML monitoring and feeds intelligence into the dispute resolution workflow, creating a connected compliance and security ecosystem rather than a collection of siloed tools.

If KYC is where the customer relationship begins, dispute resolution is where it survives or ends. And right now, for most banks and fintechs, the dispute resolution process is one of the most expensive, slowest, and customer-damaging operational functions in the business.

A single contested transaction can involve document retrieval, merchant verification, fraud analysis, regulatory compliance review, and customer communication across multiple disconnected systems and multiple teams, creating fragmented customer interactions and financial interactions before a resolution decision is reached. For institutions handling high dispute volumes, the fully-loaded cost per resolved case regularly runs into hundreds of dollars. Resolution timelines extend to days or weeks. And the customer experience during that process is, almost universally, a churn risk.

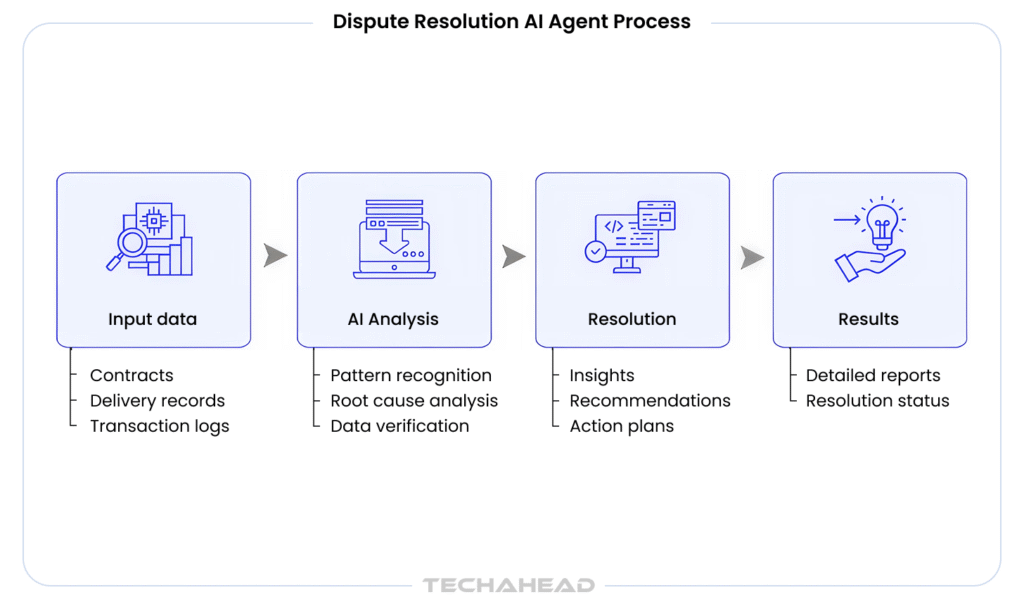

This is not a single-agent problem. A single AI agent tasked with managing the entire dispute resolution workflow becomes so generalized across its functions that it becomes unreliable in each one. The architecture that actually works for production-grade dispute resolution in fintech is a multi-agent AI system, where specialized agents each own their part of the process and an orchestration layer coordinates them as a cohesive resolution engine.

Also Read: Multi-Agent Orchestration

Here is what that architecture looks like in practice:

The result is not just faster resolution. It is defensible resolution while improving operational efficiency in dispute handling. Every decision is documented, every step is traceable, and the compliance team has a complete audit record without building it manually from system exports and email threads.

At TechAhead, multi-agent AI systems for financial dispute workflows are architected with both dimensions in mind: the operational efficiency that makes the economics viable, and the regulatory defensibility that makes the deployment sustainable in a supervised financial environment. These are not trade-offs. They are design requirements that coexist when the architecture is correct from the start.

Bonus Read: 7 Ways Multi-Agent AI Fails in Production

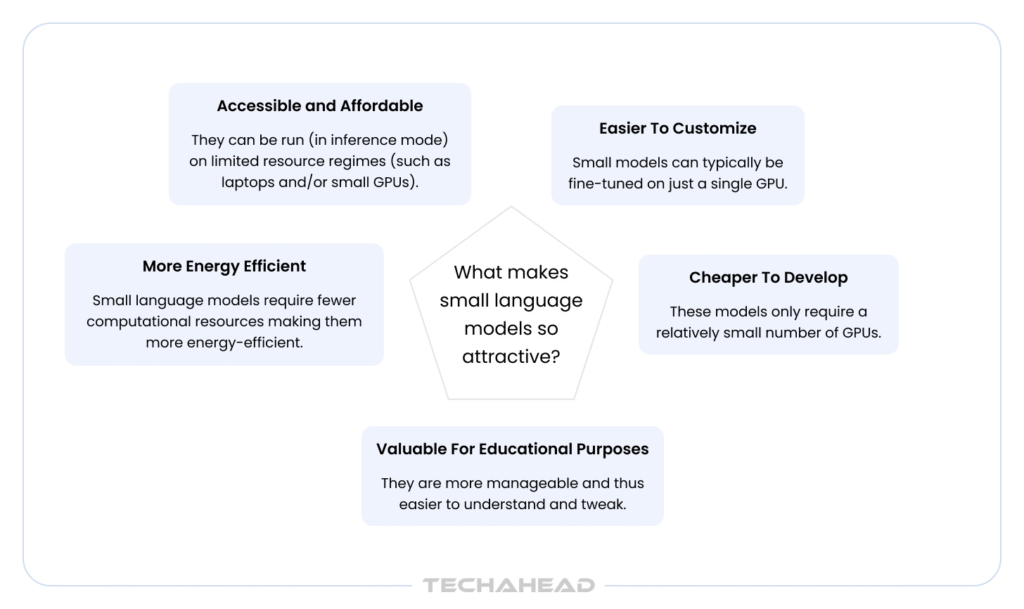

When most technology leaders think about deploying AI for risk modeling, the instinct is to reach for the most capable large language model available. Bigger model, better output. It is an understandable instinct. It is also, in the context of financial risk modeling, frequently the wrong one for financial analysis and decision-making in latency-sensitive environments.

Small language models (SLMs) for financial risk modeling outperform their larger counterparts in this specific application for three reasons that have nothing to do with raw capability and everything to do with what financial risk environments actually require:

Credit risk scoring, real-time fraud probability flagging, and portfolio stress testing all operate in latency-sensitive environments. A large language model with a multi-second inference time cannot power a risk agent that needs to evaluate a transaction in milliseconds. In payment fraud detection, latency is not a performance metric. It is the difference between catching a fraudulent transaction and processing it. SLMs are purpose-built for the inference speed that real-time financial decisioning demands.

At the transaction volumes that matter for banks and payment platforms, millions of decisions per day, the inference cost difference between a large and a small model is not marginal. It is the difference between a unit economics model that works at scale and a deployment that gets cancelled when the infrastructure bill arrives three months after the pilot. Machine learning applications in fintech at enterprise scale need economics that hold up as volume grows, not just when volume is controlled.

Regulators and internal risk committees need to understand why a risk decision was made, not just what the decision was. Smaller, domain-tuned models produce more interpretable reasoning paths. They are easier to audit against historical performance, easier to validate against regulatory expectations, and easier to defend when a credit examiner or a risk committee chair asks for a plain-language explanation of a specific decision.

Where SLMs deliver the clearest advantage in fintech risk applications:

The architecture question – large language model, small language model, or a hybrid approach where each plays its correct role – is one TechAhead evaluates specifically for every financial risk modeling engagement. There is no universal answer. But there is a principled framework for making it, including when agents should execute trades automatically only within predefined risk limits, and “use the biggest available model” is rarely the correct outcome of that framework in a regulated, latency-sensitive, high-volume financial environment.

Of all the AI agents fintech use cases in this guide, explainable AI for lending sits at the most demanding intersection: the highest technical requirements, the most acute regulatory risk, and the greatest downstream impact on customers whose financial access depends on the quality of the decision. In lending, finance AI agents must support regulated decisioning with clear controls, and the same discipline applies when firms extend AI solutions into tightly bounded personalized financial services or investment services.

Here is the core problem. AI-powered lending decisions are faster, more consistent, and when built correctly, more accurate than human underwriters operating on instinct and spreadsheets. But they create a regulatory accountability gap that regulators on both sides of the Atlantic are actively closing.

The regulatory pressure is now structural and accelerating:

What explainable AI for lending and credit decisions actually means in practice is not a model transparency dashboard that data scientists can read. In concrete terms, it means:

This is not something you retrofit onto a working lending AI system after the build. The architecture of explainability cannot be layered on top of a black box. TechAhead builds explainable AI for lending and credit decisions as a first-principle architecture requirement:

The business case for explainability extends beyond regulatory compliance. Borrowers who receive clear, factual explanations for credit decisions are more likely to return and engage with alternative products. Lending decisions with documented rationale are faster to defend in consumer disputes.

Explainable systems can also support personalized financial advice or personalized financial guidance when recommendations are clearly bounded and documented. And firms that can demonstrate robust explainable AI practices to regulators are building a trust asset with regulators and customers simultaneously – one that compounds in value as scrutiny of AI-powered financial decisions intensifies.

AI agents can perpetuate biases if trained on flawed data, which is why ethical concerns and ethical considerations must be built into governance. Near the end of the process, they can also analyze vast datasets for credit scoring more consistently than manual review, provided data quality and fairness controls are in place.

Must Read: Responsible & Ethical AI

| Fintech Function | What AI Agents Replace | Core Outcome |

| KYC and Customer Onboarding | Manual identity verification and document review | Days-to-minutes onboarding with full compliance documentation |

| AML Monitoring | Rule-based alert systems drowning teams in false positives | Typology-aware detection with audit-ready SAR generation |

| Fraud Detection | Reactive post-transaction flagging | Real-time fraud probability scoring before authorization |

| Dispute Resolution | Manual cross-system investigation and documentation | Orchestrated multi-agent resolution with complete audit trail |

| Risk Modeling with SLMs | Slow, expensive LLM inference on high-volume decisions | Millisecond risk decisioning at enterprise-grade economics |

| Explainable AI for Lending | Black-box credit decisions with no regulatory defensibility | Traceable, factor-level decision rationale satisfying CFPB and EU AI Act |

Here is the conversation that most content on AI agents fintech refuses to have: what does production-grade architecture actually look like, what are the technology decisions that determine success or failure, and what does it realistically cost to build a fintech AI agent that works?

The architecture decisions made before the first line of code is written determine whether a fintech AI agent reaches production or becomes a post-mortem agenda item.

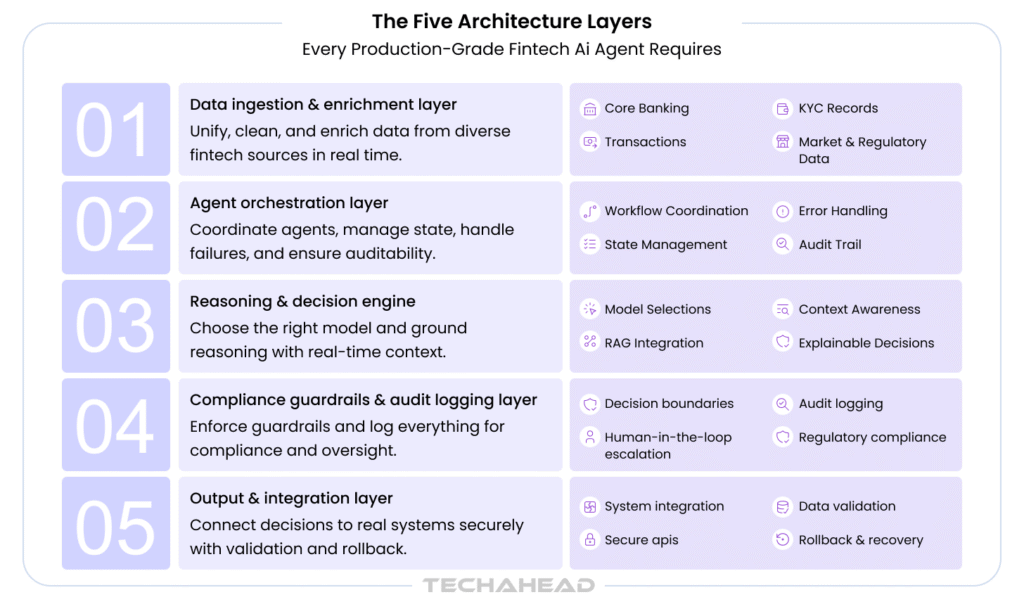

1. Data Ingestion and Enrichment Layer

An AI agent reasons only as well as the data it operates on. In fintech, that data lives across core banking systems, transaction databases, customer identity records, regulatory reference databases, credit bureau feeds, sanctions lists, and external market data sources. Before any agent can reason reliably, these sources need to be unified, cleaned, normalized, and accessible in real time, because poor data quality quickly degrades downstream agent reliability in financial operations and financial processes. This layer is where the majority of production failures originate. Fragmented data infrastructure does not become less fragmented when an AI agent is placed on top of it. It becomes more consequential.

2. Agent Orchestration Layer

For any multi-agent fintech workflow (KYC, AML monitoring, dispute resolution), there needs to be an orchestration layer that coordinates agent interactions, manages state across workflow steps, handles failures gracefully, and maintains the complete sequence of operations required for a regulatory-grade audit trail. This is not solved by chaining prompts in sequence. It requires deliberate orchestration architecture, with defined handoff protocols between agents, error handling that does not silently drop decisions, and state management that persists across the entire workflow lifecycle, often using AI platforms as a practical integration layer for existing systems.

Also Read: How to Evaluate and Benchmark AI Orchestrators

3. Reasoning and Decision Engine

The model selection decision lives in this layer. LLM, SLM, or a hybrid architecture based on the specific requirements of the use case for latency, inference cost, and explainability. This layer also houses the RAG (Retrieval-Augmented Generation) integration that allows agents to ground their reasoning in specific regulatory documents, institutional policy frameworks, and historical case data, rather than relying solely on model training, which ages and cannot be updated in real time. In more complex deployments, standards such as Model Context Protocol can help structure how context is shared across tools and agents.

4. Compliance Guardrails and Audit Logging Layer

In a regulated financial environment, this layer is not optional and it is not a feature to be added post-launch. Every agent decision, every tool call, every reasoning step, and every human escalation event needs to be logged with a timestamp and made retrievable on demand. The guardrails layer also enforces decision boundaries: defining precisely what the agent can and cannot do autonomously, and where human-in-the-loop escalation is required before an action is taken or a decision is finalized.

5. Output and Integration Layer

This is where agent decisions connect to real-world systems: core banking updates, customer notification workflows, regulatory filing systems, case management platforms, downstream data pipelines, and other financial systems. This layer requires banking-grade API security, data validation before any system writes are committed, and rollback capability for decisions that require human correction. The goal is to let financial services operate more autonomously without sacrificing control. An AI agent that makes a correct decision but writes it incorrectly to a downstream system has not made a correct decision.

Almost every fintech firm TechAhead works with initially frames human-in-the-loop as a limitation: a concession to regulatory caution that reduces the efficiency benefit of the AI agent. The correct framing is the opposite, because the goal is not zero human intervention but clearly scoped autonomy.

Human-in-the-loop is the feature that makes autonomous AI agents deployable in regulated financial environments in the first place. It is the mechanism by which firms can demonstrate to regulators that meaningful human oversight exists. It is the mechanism by which autonomous operating scope can be progressively expanded as performance data and trust accumulate over time, with some workflows eventually running under minimal human oversight once controls are proven. And it is the mechanism by which the inevitable edge cases, the decisions that fall outside the defined operational envelope, are handled appropriately rather than incorrectly at speed.

Architecting it correctly means three things in practice, and strong governance is what allows that autonomous scope to expand safely with minimal human intervention rather than without accountability:

The technology choices that most directly determine whether a fintech AI agent architecture reaches production and performs reliably:

Bonus Read: Open Banking API Strategy

This is the question that most content on AI agents fintech does not answer. Here is an honest framework, based on TechAhead’s enterprise AI development experience:

Small Engagement:

Single-function agent (e.g., KYC document verification, AML alert triage, or credit risk scoring for a defined product): $50,000 to $100,000. This covers use case definition and requirements, data pipeline setup for a single source system, single-agent build and testing, compliance layer with basic audit logging, integration with one downstream system, UAT, and deployment to a production environment.

Medium Engagement:

Multi-agent workflow (e.g., end-to-end KYC plus AML monitoring in an integrated workflow, or a full dispute resolution orchestration system): $100,000 to $200,000. This covers orchestration architecture design, multi-agent build and inter-agent integration, connections to multiple core systems, compliance and audit logging across the full workflow, UAT including regulatory test scenarios, and phased deployment with monitoring instrumentation.

Large Engagement:

Enterprise-wide orchestrated AI agent system (e.g., a connected AI layer spanning KYC, AML, risk modeling, and dispute resolution across a multi-entity financial institution, with governance framework and ongoing model monitoring): $200,000 to $500,000 and above. This covers full architecture design across multiple use cases and data domains, multi-environment deployment, deep enterprise system integration, a governance framework meeting regulatory standards, initial model validation, and production support with ongoing performance monitoring.

| Engagement | Scope | Example Use Cases | Investment Range |

| Small | Single-function agent, one data source, one downstream integration | KYC document verification, AML alert triage, credit risk scoring | $50,000 to $100,000 |

| Medium | Multi-agent workflow, multiple core system connections, phased deployment | End-to-end KYC plus AML monitoring, dispute resolution orchestration | $100,000 to $200,000 |

| Large | Enterprise-wide orchestrated system, multi-entity, governance framework included | Connected KYC, AML, risk modeling, and dispute resolution layer | $200,000 to $500,000+ |

These ranges are determined primarily by three variables: data complexity (how fragmented, how regulated, and how real-time the source data needs to be), integration depth (how many upstream and downstream systems the agents connect to and how those connections are governed), and compliance requirements (the number of regulatory frameworks the agents must operate within simultaneously, and the auditability standards each requires).

Across fintech AI engagements spanning digital lending platforms, challenger banking infrastructure, and payment systems, TechAhead has navigated the precise combination of data complexity, compliance depth, and integration scope that these cost ranges reflect.

“The fintech teams that build AI agents that actually reach production treat compliance as an architecture input, not a legal review at the end. When TechAhead starts a fintech AI engagement, we are asking the compliance questions in week one — because the answers change everything from data pipeline design to model selection to how the audit log is structured. Building compliance in is a fraction of the cost of retrofitting it six months later when the pilot is trying to scale.”

— Deepak Sinha, CTO, TechAhead

Before the architecture discussion. Before the cost conversation. Before you evaluate a single vendor or assign a single internal resource, there is a foundational decision that most financial institutions get to last when they should get to it first: are you building this internally, buying a pre-built solution, or partnering with a specialist development firm? That decision gets harder when integrating AI agents into existing financial systems becomes the core implementation challenge rather than the model itself.

Each path has a legitimate use case. Each also has a failure mode that is specific and predictable.

Build internally:

Buy a pre-built vertical solution:

Partner with a specialist development firm:

For majority of agentic AI development methodologies, the partnership model delivers the fastest path from requirements to production. TechAhead operates exclusively in this model – co-architect from day one, accountable through deployment, not handing over a codebase and stepping away.

The six fintech functions covered in this guide are not independent investments to be evaluated separately and implemented in isolation. They are components of a connected fintech AI agent layer that, in the fintech industry, can reshape the broader financial industry when built correctly and integrated thoughtfully, becoming one of the most durable competitive assets a financial institution can hold:

The financial institutions that have connected these functions are not just running more efficient operations. They are building a compounding advantage. Every quarter of operational data makes their agents more accurate. Every regulatory examination they navigate with documented AI decision trails builds institutional confidence and regulatory credibility.

The fintech leaders who succeed with fintech AI agent deployments in the next 18 months will not be the ones with the most ambitious strategies. They will be the ones who turned strategy into production-grade engineering, with a build partner who understands the difference between a demo and a system that works under real regulatory, operational, and competitive pressure.

The question for your organization is not whether to build vertical AI agents in fintech. That question is settled. The question is who builds them with you, and whether that partner has what it takes to close the distance between where your AI strategy is today and where your competitors are building toward right now.

Most development partners present credentials during the sales process and return to them only if an audit requires it. TechAhead’s credential stack is a delivery standard, not a proposal attachment. What each certification represents in the context of a fintech AI development is specific and verifiable:

Institutions like AXA, American Express, and RaspberryFX represent the most demanding end of the fintech enterprise environment. The fact that they have built with TechAhead is less a reference and more a confirmation that the delivery model holds under conditions most engagements do not face. That is the standard every fintech AI development is held to, regardless of where a client sits on the institutional complexity spectrum.

If your fintech AI initiative is moving from evaluation to execution, TechAhead’s enterprise delivery team is available to assess your requirements and identify where the highest-value deployment opportunities lie. Contact TechAhead to start that conversation.

Vertical AI agents in fintech are purpose-built for specific financial functions including KYC, AML, lending, and dispute resolution, with domain-specific training, regulatory context retention, and built-in auditability. They rely on advanced ai models tailored to regulated financial systems. Generic AI models lack these properties and cannot operate reliably in regulated financial environments.

Yes, but only when compliance is an architecture input, not an afterthought. Production-grade AI agents for financial services are built with audit trails, explainable decision logic, and governance frameworks that satisfy BSA, FATF, CFPB, and EU AI Act requirements from day one.

RPA executes predefined workflows on structured inputs. Agentic AI reasons through unstructured data, adapts to context, and handles exceptions independently, going beyond narrower ai tools and closer to autonomous systems. In fintech, RPA handles predictable automation while AI agents handle complex, judgment-based workflows like AML monitoring and KYC review.

At minimum: defined decision boundaries for autonomous vs human-approved actions, real-time monitoring, complete audit trails for every agent action, and model versioning for regulatory traceability. Most institutions currently lack mature governance, which is precisely where most deployments stall before production.

Explainable AI for lending and credit logs every step of the decision reasoning process, not just the output. When a loan is denied, the system produces a documented rationale with specific factors, not just a model score, satisfying CFPB adverse action requirements and fair lending examination standards.

Production-grade fintech AI agents process customer financial data within banking-grade security controls including encryption in transit and at rest, role-based access, and defined retention policies. Strong controls are essential because data privacy violations can carry major penalties, and autonomous software systems may introduce new vulnerabilities if not properly governed. SOC 2 Type II and ISO 42001 certification on the development side validates these controls through independent audit.

By analyzing behavioral context across transaction histories, counterparty networks, and entity relationships simultaneously rather than applying fixed thresholds to individual transactions. AI-powered AML agents adapt to emerging typologies, prioritize alerts by risk materiality, and generate audit-ready SAR narratives automatically.

No, and regulators expect the opposite. Human-in-the-loop is an architecture requirement in fintech AI development, not a limitation, even if bounded workflows can reduce human intervention to minimal human oversight. Well-built agents define precise escalation triggers and expand autonomous operating scope progressively as performance data and regulatory confidence accumulate over time.

Because dispute resolution involves multiple distinct functions including intake, evidence retrieval, regulatory reasoning, documentation, and customer communication, each requiring specialized logic. A single generalized agent becomes unreliable across all five. Multi-agent AI systems assign each function to a specialized, coordinated agent.

ISO 42001:2023 for AI management systems, SOC 2 Type II for continuous data security assurance, and AWS or Azure partner status with security competency designations. These are not just credentials. They are verifiable delivery standards that directly govern how a regulated fintech AI engagement is built and audited.

Let’s evaluate your readiness and calculate your score in minutes

We use cookies to ensure our website functions properly, improve performance, and provide a personalized experience. You can choose which types of cookies to allow below.

Required for core functionality such as security, network management, and accessibility. These cannot be disabled.

Help us understand site traffic and user interactions so we can improve performance and usability.

Enable enhanced functionality and personalization such as language or region preferences.

Used to deliver relevant ads, track campaign performance, and measure advertising effectiveness.