Copy Link

Copy Link Share on X

Share on X Share on Facebook

Share on Facebook Share on LinkedIn

Share on LinkedIn

Always Active

Required for core functionality such as security, network management, and accessibility. These cannot be disabled.

Uncover the transformative potential of digital and mobile solutions for your industry.

Last Updated: Aug 4, 2026

Jun 12, 2026

Last Updated: Aug 4, 2026

Jun 12, 2026  313

313  26 min. Read

26 min. Read

Key Takeaways

Let’s evaluate your readiness and calculate your score in minutes

Between 85 and 95 percent of AML alerts generated by rule-based transaction monitoring systems are false positives. That single figure carries a significant operational weight: compliance teams at most financial institutions spend the majority of their investigative capacity confirming that flagged activity was legitimate, not pursuing the financial crime patterns that actually require reporting. The monitoring architecture producing that outcome has not fundamentally changed in over a decade. The financial crime environment it was built to detect has.

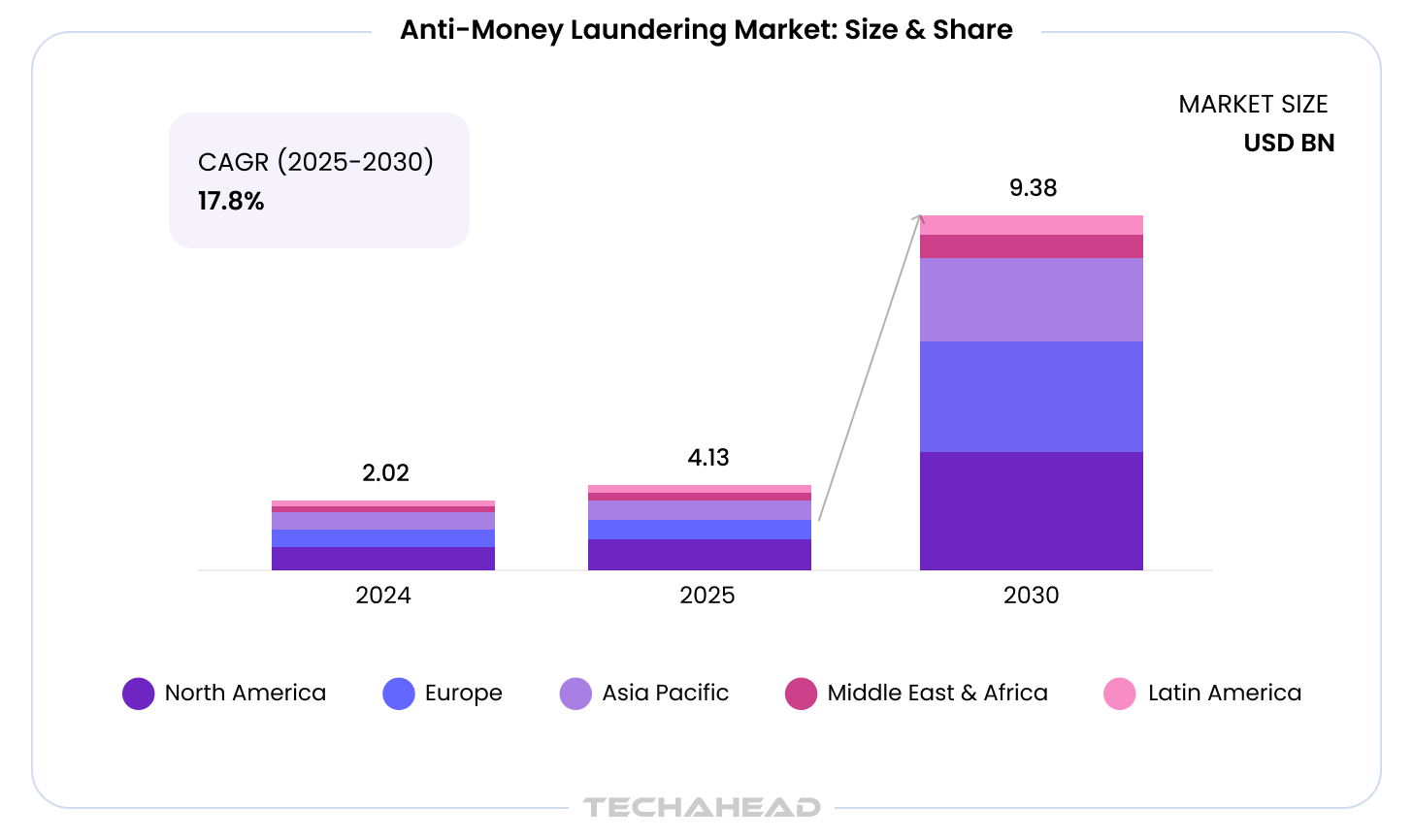

That is not a staffing problem. That is a system design problem. According to MarketsandMarkets, the global anti-money laundering solutions market is projected to grow from $4.13 billion in 2025 to $9.38 billion by 2030 at a 17.8 percent CAGR, driven by rising transaction volumes, expanding financial crime threats, and regulatory demand for monitoring technology that can keep pace with both.

In 2026, the distance between financial firms still running legacy rule-based AI AML monitoring and those that have deployed purpose-built AI agents is showing up in real numbers: examination outcomes, SAR quality, investigation costs, and the rate at which genuine financial crime slips through what everyone optimistically called a monitoring program.

This piece is for business owners and technology leaders who are past the question of whether AI can fix the false positive problem. The question you are actually navigating is: what does it look like in production, where has it proven out in documented deployments, and what does it take to build correctly so it holds up under BSA examination?

Must Read: Vertical AI Agents in Fintech: The Enterprise Leader’s Guide

The most consistently documented failure in BSA compliance operations is also the one most financial firms have accepted as the cost of doing business. Financial crime compliance research, including the Everest Group’s 2025 AML benchmarking, puts the false positive rate for rule-based anti-money laundering (AML) transaction monitoring systems at between 85 and 95 percent of generated alerts. The overwhelming majority of cases reaching a compliance analyst for review represent legitimate customer activity, meaning legitimate transactions were being incorrectly flagged.

The operational consequence is also not abstract. A mid-sized bank processing 1,000 AML alerts per day at Level 1 review times of 30 to 45 minutes per alert is consuming up to 700 analyst hours daily to confirm that flagged activity was legitimate. That capacity is not applied to the genuine suspicious activity moving through undetected, in patterns the rules were not written to recognize.

That second failure is the one compliance teams feel most acutely during examinations: false negatives. When analysts spend the bulk of each review cycle clearing legitimate activity, investigations that require genuine depth get compressed. The financial crime patterns most likely to pass through undetected are:

The 90 to 95 percent false positive rate and the false negative problem are not separate failures. They are two outputs of the same system design flaw. Any solution that addresses only one while worsening the other is not a solution. The instinctive response is threshold calibration: adjusting rules to shift alert volume while trying to preserve detection sensitivity. That instinct treats the false positive crisis as a precision problem. It is a design problem.

Must Read: Agentic AI Development Guide

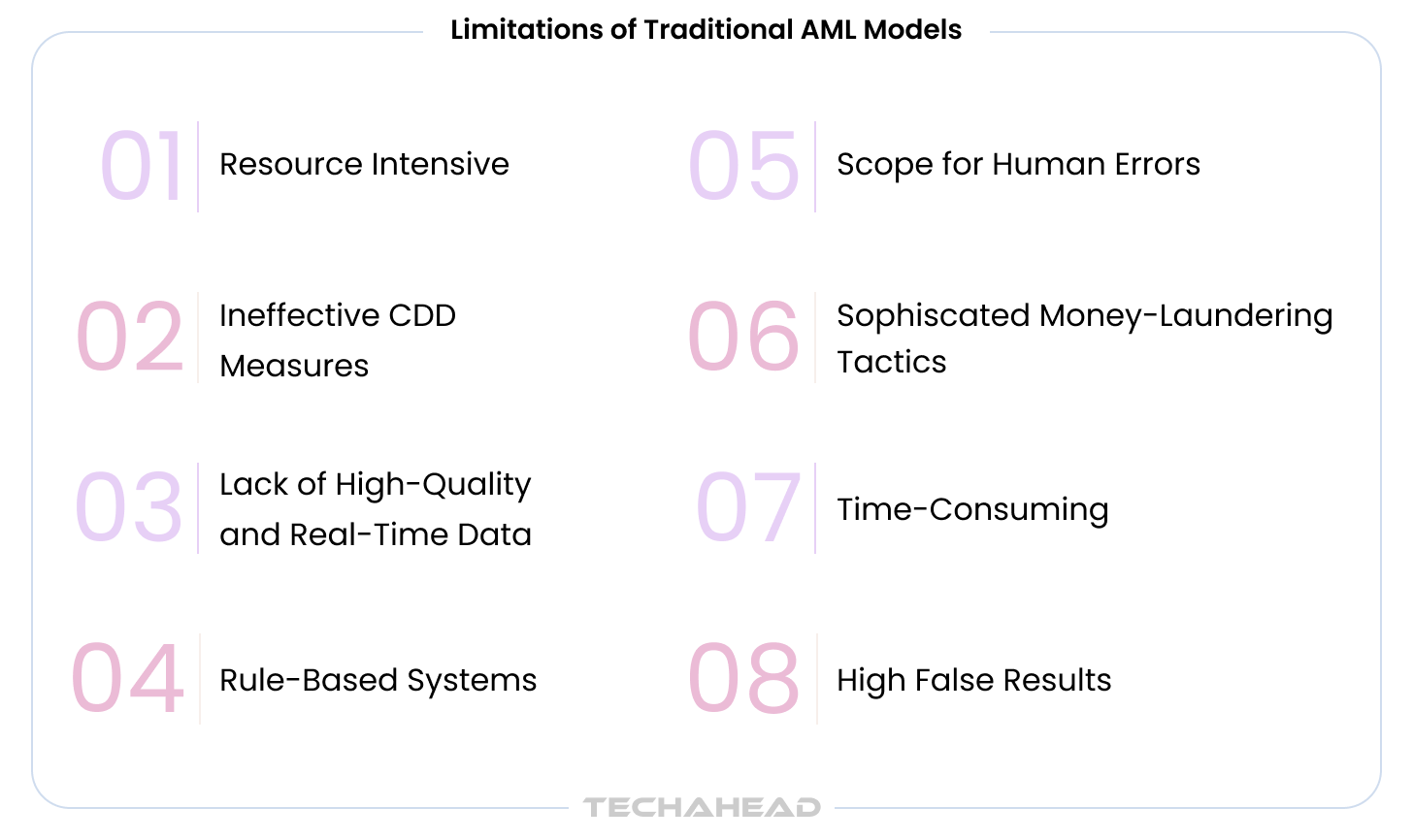

Rule-based AML transaction monitoring was built on a core assumption: that suspicious activity is identifiable by applying fixed criteria to individual transactions in isolation. In traditional rule-based systems, traditional systems rely on fixed rules and thresholds rather than adaptive context. That assumption was designed for a financial crime environment that no longer exists.

What rule-based systems structurally cannot do:

Lowering a threshold increases false positives. Raising it misses genuine activity. AI-based monitoring aims for fewer false positives and fewer false-positive alerts while preserving risk detection. Neither corrects the underlying structural limitation. The only correction is an architecture that was designed to reason about transaction risk in context rather than apply fixed rules to isolated events.

Bonus Read: Agent2Agent Architecture (Era of Agent Collaboration)

| Dimension | Rule-Based AML | AI Agent AML |

| Alert Trigger | Fixed thresholds on individual transactions | Behavioral risk scoring across customer history, context, and counterparty networks |

| False Positive Rate | 85–95% industry average | 40–65% lower in documented deployments |

| False Negative Risk | High; sophisticated laundering patterns often missed | Lower; detects hidden relationships and behavioral anomalies across entities |

| Typology Adaptation | Manual rule creation and updates | Continuous learning from investigations and analyst feedback |

| SAR Generation | Manual narrative drafting and evidence collection | AI-assisted SAR drafting with pre-assembled evidence, subject to human review |

| Audit Trail | Basic activity and alert logs | Timestamped decision rationale with full traceability for regulators |

| Cross-Entity Detection | Limited to predefined rule parameters | Network analytics across accounts, counterparties, products, and jurisdictions |

There is a meaningful distinction between applying machine learning to transaction monitoring and deploying an AI agent framework across a BSA compliance program. A machine learning AML model improves the pattern recognition accuracy of a single monitoring function, while AI models support that narrow use case and AI systems coordinate the broader workflow. An AI agent architecture transforms the entire workflow, from alert generation through case investigation through SAR filing, as a coordinated, auditable, continuously learning system. Behavioral analysis in production programs can reduce false positives by 70-90%.

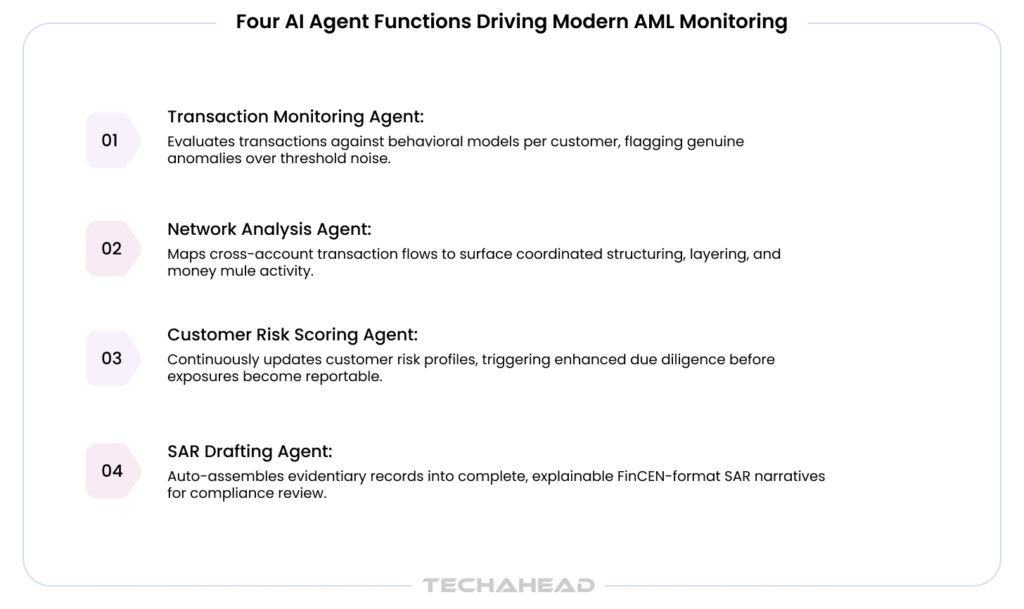

AI agents for AML monitoring in a production BSA program operate across four coordinated functions:

Analyzes incoming transactions to monitor transactions continuously against a maintained behavioral model for each customer rather than only checking fixed thresholds, applying behavioral analytics and anomaly detection to evaluate transaction size, frequency, timing, counterparty characteristics, geographic patterns, and channel behavior simultaneously. The output is a risk probability score reflecting full behavioral context for suspicious transactions and transactional risk: whether the transaction is consistent with that customer’s established patterns and whether it resembles any documented AML typology cluster. Transactions within normal behavioral range are auto-cleared with a logged reasoning trail. Elevated-risk transactions escalate to the case orchestration layer with supporting evidence already assembled. The agent also distinguishes legitimate financial transactions from those that warrant escalation, supporting fewer false positives.

Also Read: Multi Agent Orchestration

Financial crime does not operate in single accounts. Structuring, layering, and money mule operations involve coordinated behavior across multiple accounts and entities, each of which may look individually normal. The network analysis agent helps identify patterns across multiple accounts and entities by mapping transaction flows across counterparty relationships, identifying unusual clustering patterns to support anomaly detection for emerging threats, surfacing shared device and IP activity across accounts, and detecting transaction chains designed to obscure the origin of funds. This financial crime detection capability through cross-entity visibility is structurally unavailable in any single-transaction rule-based system, and it is precisely where the false negative problem concentrates, exposing risks such as actual money laundering activity and terrorist financing.

Related: Real Time Fraud Detection at Scale

Rather than applying a static risk rating at onboarding and revisiting it on an annual schedule, the risk scoring agent updates customer risk profiles continuously to flag high risk customers based on evolving transaction behavior, new counterparty relationships, adverse media signals, and changes in account usage, with AI tools analyzing structured and unstructured data, including unstructured data from adverse media and investigator notes. Material risk profile shifts trigger enhanced due diligence review before suspicious activity builds into a reportable exposure. AI enhances Customer Due Diligence by automating identity verification processes.

When a case crosses the filing threshold, the drafting agent assembles the full evidentiary record and generates a Suspicious Activity Report (SAR) narrative in FinCEN format, supporting more accurate suspicious activity reports. SAR automation through AI agents reduces documentation burden, and explainable AI helps show why a case was flagged, allowing compliance teams to review stronger filings instead of piecing them together from case notes and transaction exports. Compliance officers review a structured, complete filing rather than building one from case notes and transaction exports. The human review step before any SAR is filed is not procedural formality. It is the control that prevents AI-generated narratives from introducing hallucinated facts or omitting critical details that would weaken the filing under regulatory scrutiny, while clearer explanations help compliance teams and regulatory bodies review filings more efficiently.

The non-negotiable architecture requirement across all four agents: every decision must be fully logged, timestamped, and retrievable on demand. Not as a logging add-on installed after the system is in production. As a design requirement that shapes how each agent reasons from the first architecture session. When a BSA examiner asks why a specific alert was cleared eight months ago, the answer needs to come from the audit trail, not from institutional memory or reconstructed case notes.

The regulatory developments of 2025 and 2026 are not background context for AI AML adoption. They are build specifications. What U.S. regulatory bodies including FinCEN, the OCC, and the Federal Reserve have signaled in the past twelve months defines what an AI AML system must produce, document, and demonstrate to satisfy current regulatory requirements, support regulatory compliance, and hold up under BSA examination. Getting the build wrong is not a compliance risk that can be remediated after deployment. It surfaces during the next examination cycle.

Three developments define the current build standard:

Treasury Under Secretary John Hurley signaled the adoption window is open at ACAMS Las Vegas in September 2025, stating that institutions using AI to reduce false positives “should not be penalized for what the AI solution uncovers about previous gaps in their AML process.”

What gets built during that window, however, needs to hold when regulatory expectations formalize. BSA compliance AI that produces lower false positive rates, defensible SAR narratives, and institution-owned governance documentation simultaneously is not an aspirational outcome. It is the build standard.

When a global payment services client operating under active BSA examination needed its alert adjudication layer rebuilt, TechAhead structured every regulatory documentation requirement as an architecture input on day one, not a compliance task to be addressed before the next examiner visit.

Related: EU AI Act Compliance Checklist

The case for AI transaction monitoring in AML and BSA compliance programs does not rest on projections. Documented production deployments at major financial institutions show consistent, verifiable results across different institution types, geographies, and transaction volumes.

Four of the most credible documented examples of AML false positive reduction in production follow, showing how AI powered AML solutions perform in real environments, each with source references for your independent verification. AI systems improve detection capabilities while reducing operational costs in AML compliance.

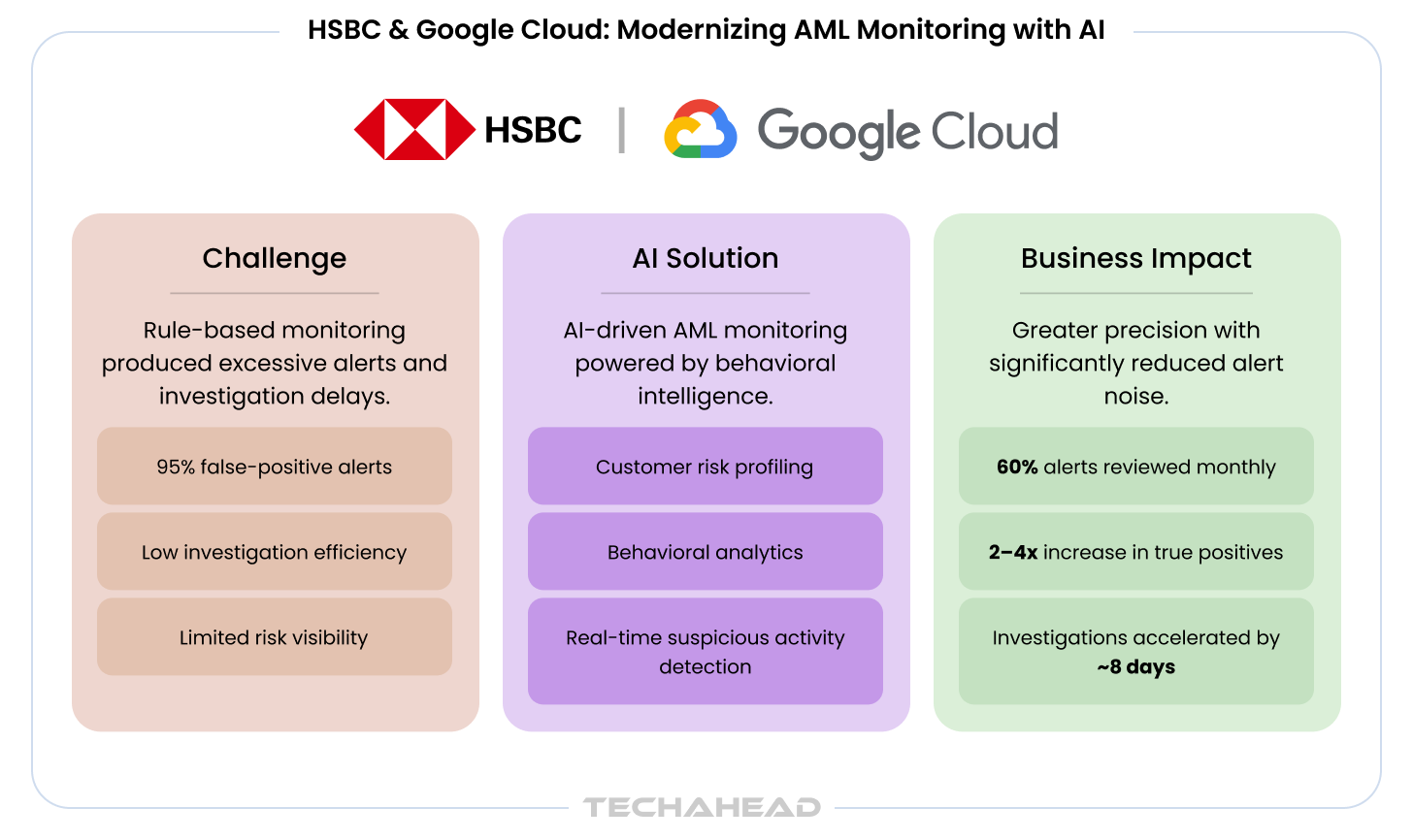

The problem: HSBC’s rule-based AML transaction monitoring across retail and commercial operations generated alert volumes that imposed significant cost and analyst fatigue at scale. More than 95 percent of system-generated alerts were confirmed false positives at the first phase of review, with approximately 98 percent never culminating in a SAR filing, a figure documented in the Google Cloud program launch press release.

What was deployed: HSBC adopted Google Cloud’s AML AI as its primary AI-based transaction monitoring system in key markets, integrating with existing systems and modernizing legacy systems while replacing the rule-based approach with machine learning AML models generating a consolidated customer risk score built on transaction data, KYC records, account behavioral history, and prior suspicious activity patterns. Rather than matching individual transactions against static rules, the system evaluated risk across the full customer behavioral profile in real time.

The result: 60 percent reduction in alert volume, alongside a 2 to 4 times increase in true positive detection, simultaneously eliminating false positive noise and catching significantly more genuine suspicious activity the rule-based system had been missing entirely, which improved operational efficiency for compliance teams. Investigation timelines came down from weeks to approximately eight days. HSBC’s group head of financial crime risk and compliance described the outcome as “a fundamental paradigm shift in how we detect unusual activity in our customers and their accounts.”

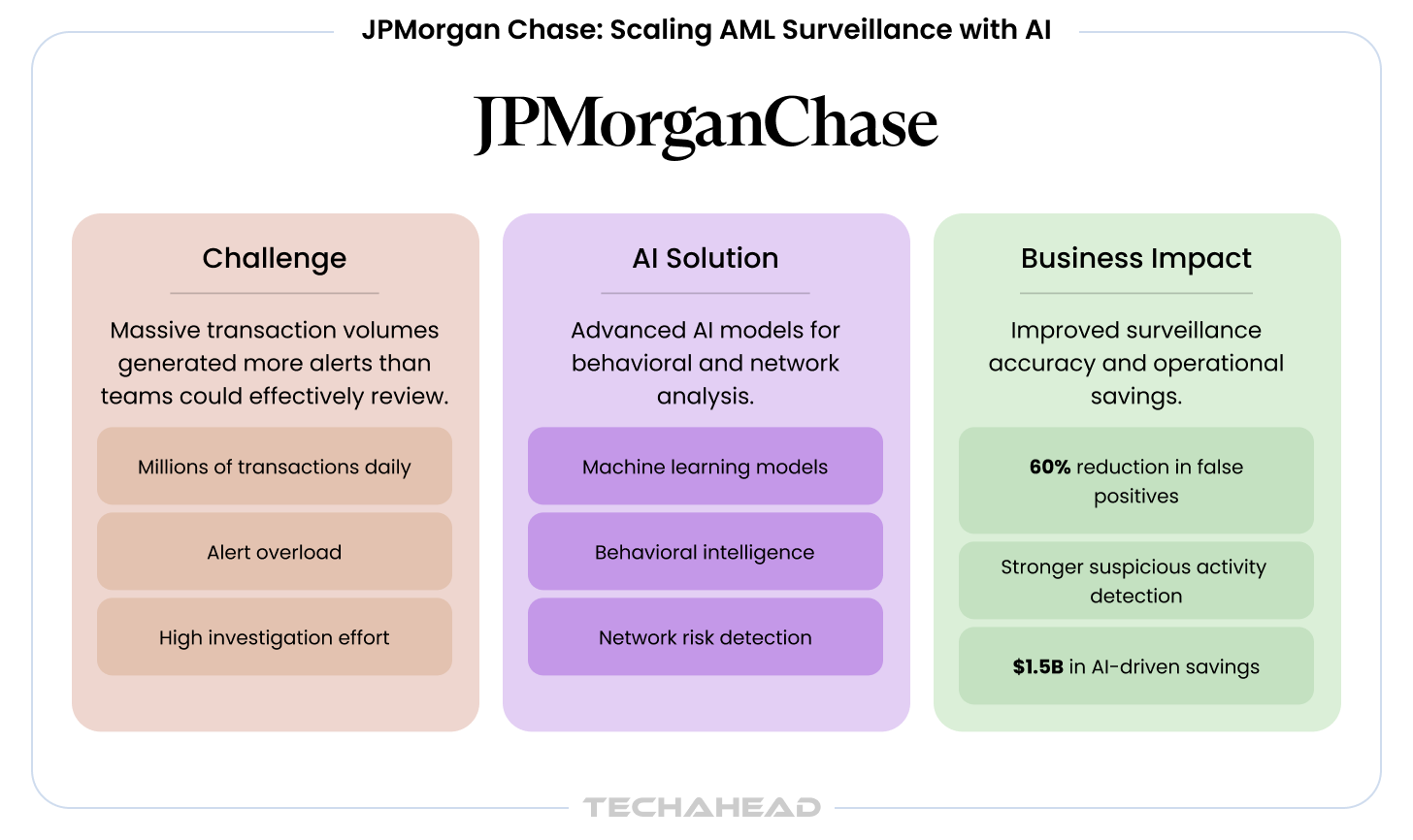

The problem: JPMorgan Chase, the largest US bank by assets, processes millions of transactions daily across consumer, commercial, and investment banking operations. At that transaction volume, rule-based AML systems generate alert queues that outpace any practical human review capacity, with genuine suspicious activity patterns obscured inside high-volume false positive noise.

What was deployed: JPMorgan deployed AI models including machine learning models and graph neural networks, plus AI tools working across AML processes, analyzing behavioral signals at the transaction level and mapping counterparty networks to detect coordinated activity patterns that individual transaction rules cannot surface.

The result: Approximately 60 percent reduction in false positives in AML surveillance, supporting risk mitigation and better management of AML risks, as reported in analysis of JPMC’s 2024 AI performance data. AI investments across fraud prevention and financial crime compliance contributed to approximately $1.5 billion in AI-driven cost savings documented in 2024.

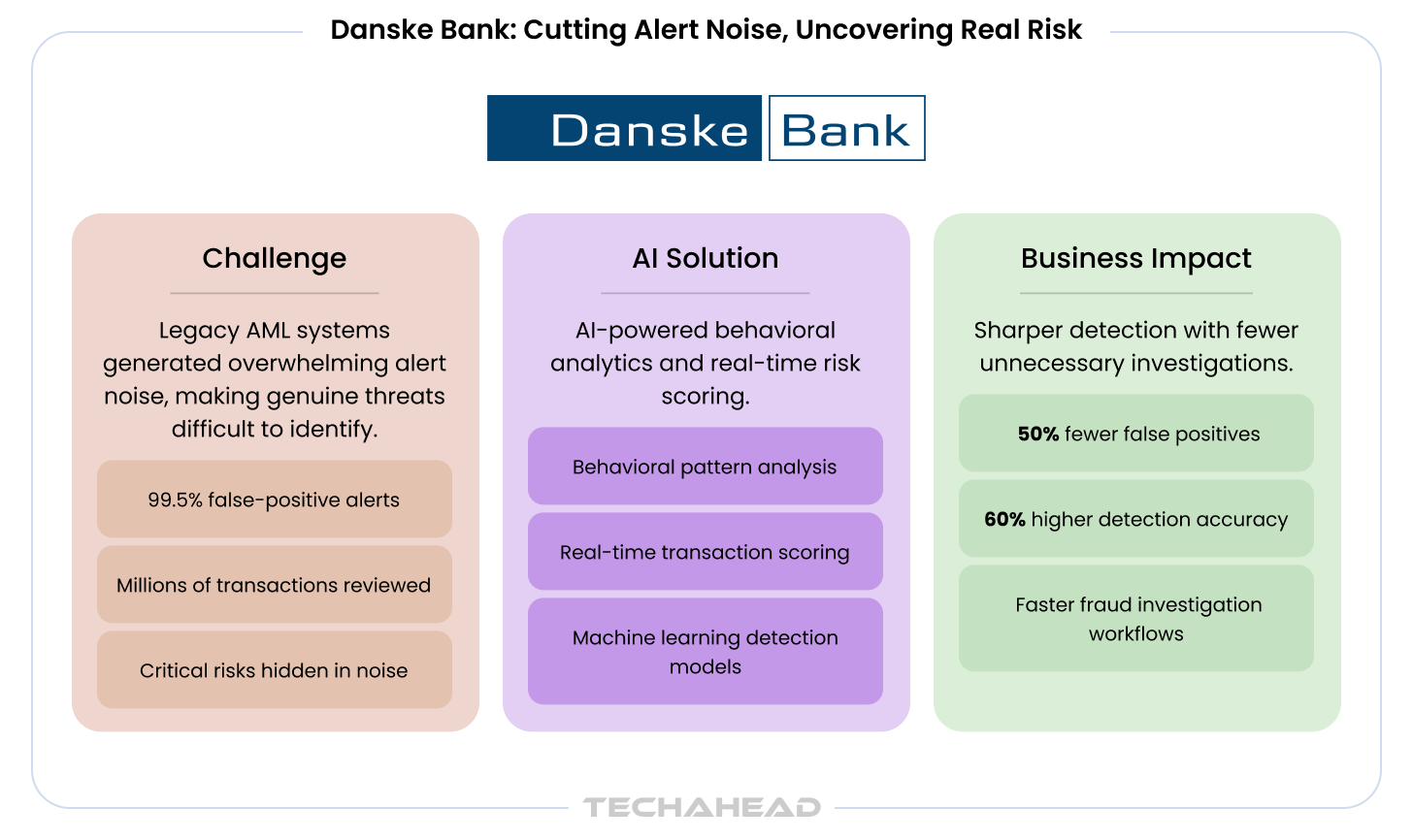

The problem: Danske Bank’s legacy AML and fraud detection system ran on handcrafted rules accumulated over years of compliance operations, where traditional systems rely on static approaches that struggled to adapt. At peak transaction volume, its false positive rate reached 99.5 percent, meaning for every 200 flagged transactions, one represented genuine suspicious activity. Investigation costs were unsustainable and actual financial crime signals were effectively invisible inside the alert noise.

What was deployed: As part of the bank’s AI implementation, machine learning ensemble models analyzed tens of thousands of behavioral features across millions of transactions in real time, with model performance dependent on data quality and stronger detection accuracy supported by cleaner inputs. Each transaction was scored in under 300 milliseconds, enabling risk decisioning at the point of transaction rather than in overnight batch processing runs.

The result: 50 percent reduction in false positives alongside a 60 percent increase in detection rate for genuine suspicious activity, as documented in the official Teradata implementation announcement and confirmed directly by Nadeem Gulzar, Danske Bank’s head of advanced analytics. The institution described the outcome as a system providing “immediately actionable insight regarding true, and false, fraudulent activity,” a functional shift from an alert queue that had been operationally impossible to process effectively.

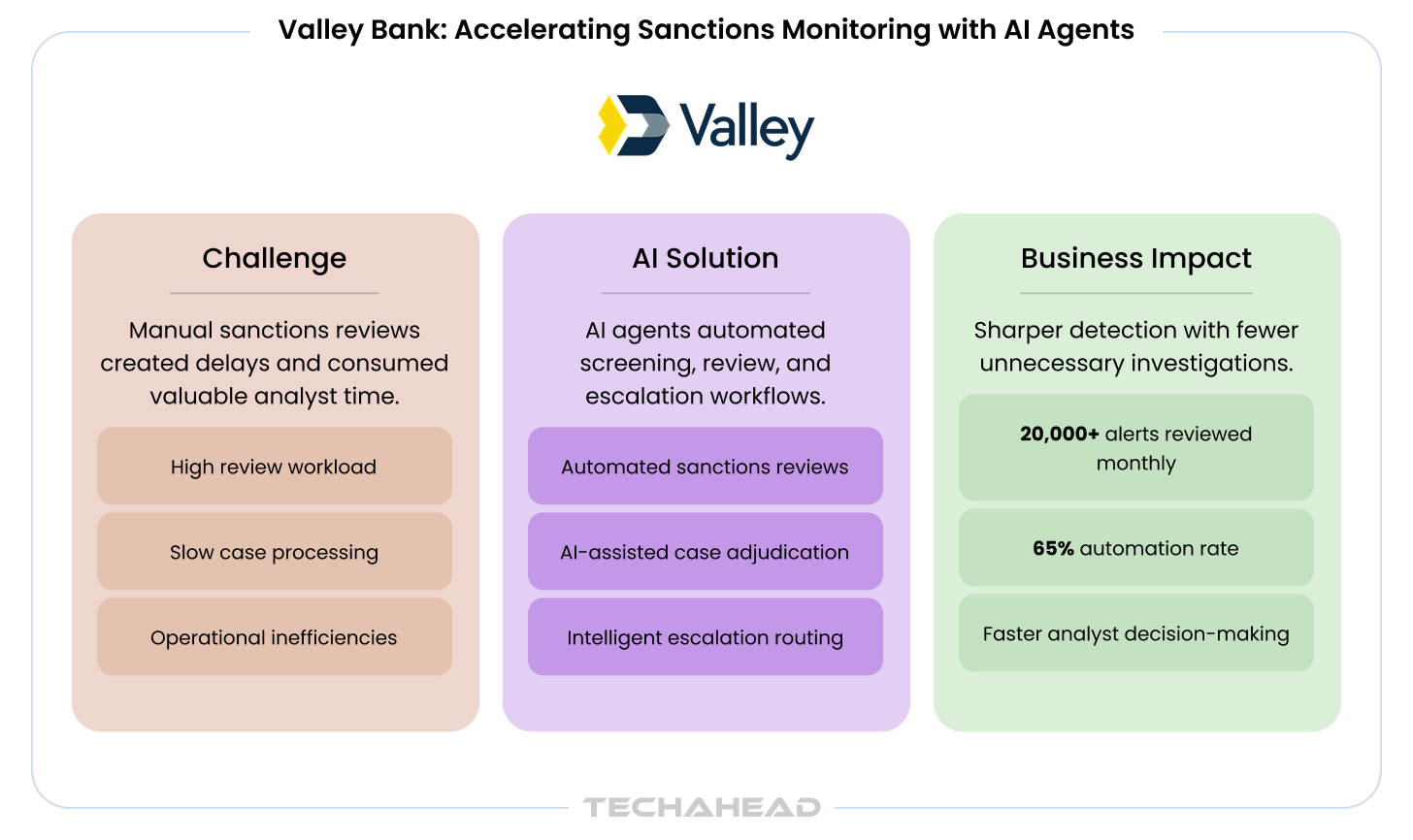

The problem: Valley Bank, a US regional bank with direct BSA and OFAC compliance obligations, faced the alert adjudication challenge common across institutions operating real-time payment rails: a high volume of sanctions screening alerts requiring Level 1 analyst review, with most representing false positive name matches that consumed compliance team capacity without actionable findings.

What was deployed: An AI agent purpose-built to automate sanctions alert adjudication in real time, designed to replicate the evaluation logic of a trained Level 1 BSA analyst. During rollout, the agent handled alerts alongside existing systems, supporting risk mitigation while it reviewed each case against counterparty data, transaction context, and screening parameters, then either cleared it with a documented reasoning trail or escalated it to a human reviewer with the full case file pre-assembled.

The result: Automated review of over 20,000 alerts per month, achieving a measurable AML false positive reduction through a 65 percent automation rate for sanctions alert adjudication. This helped by allowing compliance teams to focus on escalated cases requiring genuine judgment and improved operational efficiency. The bank reported faster payment processing and improved compliance team capacity as direct operational outcomes.

For compliance and technology leaders evaluating the build decision, it is important to understand what production-grade AML compliance automation actually requires before vendor or development partner evaluation begins. AI development services for regulated financial institutions should address the complete architecture—not only model selection, but also data integration, auditability, governance, and human oversight.

AI models are only as good as the data they operate on, and high-quality data is required for accurate results. A production AML agent requires unified access to structured and unstructured data, including transaction records, customer identity data, counterparty information, KYC documentation, sanctions databases, adverse media feeds, and behavioral history. Fragmented data infrastructure does not improve when an AI layer is placed above it. It becomes more consequential. The majority of production failures in AML AI originate in data integration, not in model selection, because poor data quality creates compliance risks as well as model-performance issues.

The models generating risk scores need to produce reasoning that can be explained to a BSA examiner, with explainable AI features in the outputs, not just statistically accurate results. In a regulated financial environment, even when a model uses capabilities such as natural language processing, its auditability and interpretability carry regulatory implications that purely technical selection criteria do not address.

The orchestration layer determines what happens after a risk score is generated. Low-risk activity is auto-cleared with a logged reasoning trail. Elevated-risk cases are assembled into complete case files before reaching the human review queue. The goal is not a smaller alert queue, it is a queue where every case reaching a compliance analyst requires analyst judgment.

Every agent decision, every alert cleared, every case escalated, every SAR narrative generated, requires a timestamped, retrievable log with the documented reasoning behind it. This cannot be retrofitted to a working system after the fact. It has to be embedded in the design from the first architecture session.

Precisely defined escalation triggers, complete case handoff to reviewing analysts, and documented human decision points allow institutions to demonstrate meaningful oversight during examination. As the system accumulates performance data, the autonomous operating scope can be progressively expanded from a documented, defensible baseline, rather than contracted under examination pressure.

“Every AML AI build we have assessed that failed under BSA examination had the same root cause: governance was treated as documentation to assemble before the audit, not design criteria to embed before the build. The institutions that got it right started with the examiner’s question. Not the engineer’s answer.”

— Mukul Mayank, Co-Founder and COO, TechAhead

Recommended: Human in the Loop AI

The use cases in the previous section are well documented and the institutions named carry significant credibility. At this point the natural next question for any compliance or technology leader is: if HSBC and JPMorgan proved this works, why not simply procure a packaged AML platform rather than commission a custom build?

It is a reasonable question. The answer is specific, not theoretical.

Pre-built AML platforms are engineered around an average institutional profile. Most financial institutions are not average. The gaps show up in predictable places:

A cross-border payments client came to TechAhead after a packaged AML platform could not produce examination-ready audit trails for its proprietary transaction infrastructure. TechAhead replaced it with a purpose-built agent layer that owned the complete documentation chain from alert generation through SAR filing.

A custom-built AI agent addresses each of these at the architecture stage because the build starts with your BSA program requirements, not an average institutional profile. When your program evolves across new products, new transaction types, and new FinCEN typology guidance, the system adapts to your AML processes on your timeline. The institutions whose false positive math changed materially built systems designed specifically for their data environment, their regulatory profile, and their examination history. That design specificity is not something a configuration process delivers. It requires an agentic AI development company that starts with your BSA program requirements, your data environment, and your examination history before a model is selected or a line of code is written.

“When a financial institution comes to us after a packaged AML platform failed examination, the conversation is always the same: the vendor’s audit trail answered the vendor’s questions, not the examiner’s. A BSA program is institution-specific. The system built to monitor it cannot be anything less.”

— Shanal Aggarwal, Chief Commercial and Customer Success Officer, TechAhead

Choosing the right fintech development company for a BSA compliance build is a materially different evaluation than selecting a packaged AML platform. The questions that matter are not about features or pricing tiers. They are about whether the partner has operated in regulated financial environments long enough to treat compliance requirements as architecture inputs rather than implementation checklists. For institutions including American Express, AXA, and RaspberryFX, that partner has been TechAhead, an AI engineering firm whose fintech delivery record spans financial services, insurance, and cross-border payments, each with its own compliance burden, examiner expectations, and data infrastructure constraints.

What makes that delivery record credible in a BSA context is not the client list alone. The build standard behind it is independently verified:

For institutions evaluating AI-powered AML monitoring, these credentials matter only insofar as they reflect how TechAhead builds. Every AML system is purpose-built for the institution’s specific BSA program, data environment, and examination history, with institution-owned governance, audit trail design, and SAR generation capability designed in from the first session.

If your BSA monitoring program is running on a rule-based architecture that is no longer keeping pace with your transaction volumes or examination expectations, the right starting point is a direct conversation. Talk to TechAhead’s AI team to assess where purpose-built AI agents deliver the most immediate and defensible impact on your false positive problem.

Rule-based systems apply fixed thresholds to individual transactions without any behavioral context. When every transaction above a configured size or pattern triggers an alert regardless of customer history, false positive alerts routinely hit 85 to 95 percent across most institutions, often sweeping in legitimate transactions that do not warrant escalation.

AI agents pre-assemble the full evidentiary record before a case reaches a compliance officer, generating a FinCEN-format SAR narrative directly from investigation data. Analysts review structured, evidence-backed filings rather than building SARs manually from scattered case notes.

No, and that is not the goal. AI agents handle high-volume routine alert adjudication, allowing compliance teams to focus on higher-risk cases requiring genuine judgment. The compliance team does not shrink; it shifts toward higher-value investigative work.

The revised guidance explicitly excludes agentic AI from its formal scope. Banks deploying AI agents in BSA programs must now build and document their own governance frameworks. That governance must be institution-owned, not sourced from a vendor’s documentation.

Network analysis agents map transaction flows across counterparty relationships, surface coordinated account behavior, and detect layering patterns that individually stay below every configured threshold. Behavioral analytics identifies what single-transaction rule logic was never designed to find.

Traditional rule based systems apply fixed rules to single transactions. By contrast, ai powered transaction monitoring uses machine learning to reason across behavioral histories, counterparty networks, and real-time patterns simultaneously. The distinction is not speed. It is the ability to detect financial crime that static rule logic fundamentally cannot surface.

Yes, and most institutions run both in parallel during validation. That parallel phase supports risk mitigation by measuring false positive reduction and true positive improvement against your baseline while the AI system works with existing systems before the legacy setup is fully retired.

Start with a BSA program and data readiness assessment. Before vendor evaluation begins, the institution needs clarity on alert volumes, false positive rates, examination history, and data infrastructure gaps. Those findings determine what the system actually needs to do.

Let’s evaluate your readiness and calculate your score in minutes

We use cookies to ensure our website functions properly, improve performance, and provide a personalized experience. You can choose which types of cookies to allow below.

Required for core functionality such as security, network management, and accessibility. These cannot be disabled.

Help us understand site traffic and user interactions so we can improve performance and usability.

Enable enhanced functionality and personalization such as language or region preferences.

Used to deliver relevant ads, track campaign performance, and measure advertising effectiveness.