Copy Link

Copy Link Share on X

Share on X Share on Facebook

Share on Facebook Share on LinkedIn

Share on LinkedIn

Always Active

Required for core functionality such as security, network management, and accessibility. These cannot be disabled.

Build intelligent AI systems that automate decisions, accelerate innovation, and scale business growth.

Design, build, modernize, and scale digital products that drive business growth.

Build secure, scalable, and intelligent platforms that power modern enterprises.

Build intelligent, connected, and autonomous systems that operate in the real world.

Flexible engineering capacity with predictable delivery, ownership, and outcomes.

Uncover the transformative potential of digital and mobile solutions for your industry

Last Updated: May 5, 2026

Oct 14, 2024

Last Updated: May 5, 2026

Oct 14, 2024  2528

2528  15 min. Read

15 min. Read

Key Takeaways

Over the past decade, technological advancements have catapulted fintech from the periphery to the forefront of financial services. This rapid growth has been driven by the dynamic expansion of the banking sector, rapid digital transformation, shifting customer expectations, and the strong backing of investors and regulators. Fintech companies have fundamentally reshaped financial services with their innovative, differentiated, and customer-centric solutions, agile strategies, and cross-functional expertise.

As of July 2023, fintech firms listed on the public market reached a combined market capitalization of $550 billion, double their value from 2019. At the same time, the sector boasted more than 272 fintech unicorns, collectively valued at $936 billion, a significant increase from just 39 firms five years ago.

The growth of these strategies and the swift adoption of fintech are largely driven by their ability to address critical gaps within traditional banking. Fintech companies offer more accessible, intuitive ways for consumers to control and manage their finances, providing solutions that banks have historically overlooked. Their seamless integration into everyday life, through mobile app development and web development, has significantly elevated convenience and customer engagement.

In this blog, we will explore the groundbreaking technologies shaping the future of the financial sector. We will also provide you with the overall technology trends in the finance industry that are reinventing the industry.

Banks face increasing pressure due to changing customer preferences, complex regulations, fintech competition, and rising liquidity costs. The digital transformation is rapidly reshaping the industry, pushing banks to adopt the latest technological innovations to stay competitive.

Simultaneously, regulators are placing greater emphasis on technological capabilities, with a focus on data enhancement and fintech integration. Deloitte highlights that banks must align these innovations with strategic planning and robust governance to meet regulatory expectations.

Below is an in-depth look at the trends, technologies, and challenges shaping the future of banking and fintech.

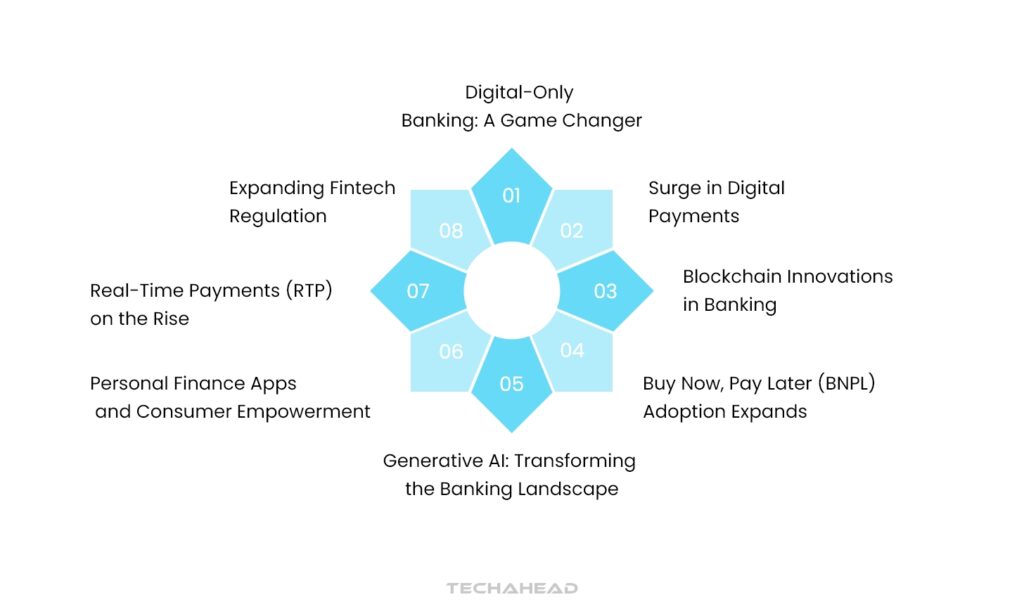

Digital-only banks, or neobanks, operate exclusively through online platforms, eliminating the need for physical branches. They offer seamless digital experiences with mobile deposits, lower fees, and competitive rates.

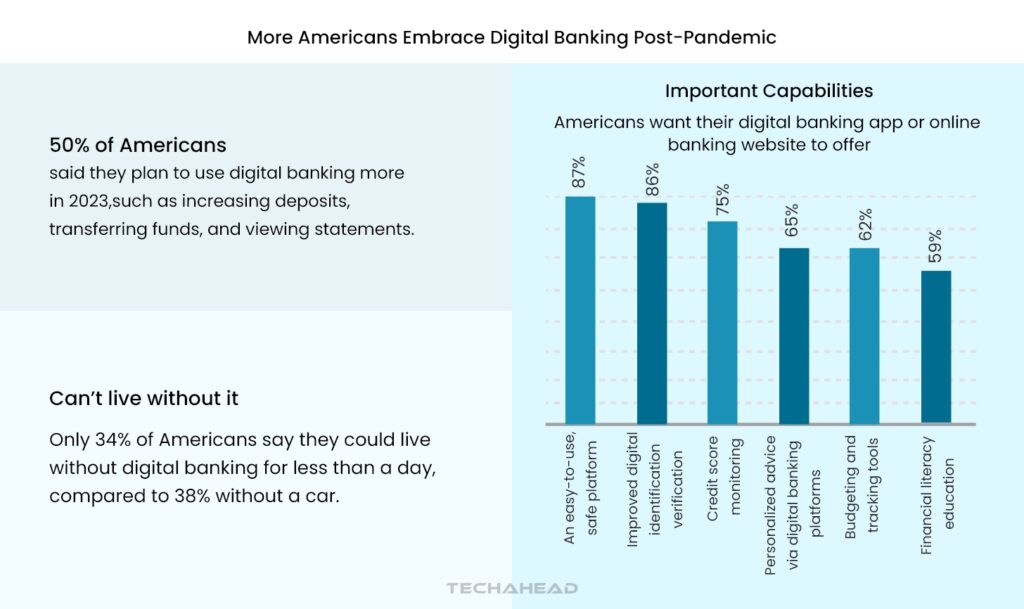

The demand for digital banking is surging as more consumers prefer efficient, on-the-go financial solutions. According to the American Bankers Association, digital banking is now preferred by 71% of consumers, with millennials and Gen Z leading the trend.

Traditional banks are facing a decline, with over 2,555 branches closing in the U.S. in 2023 alone. This shift signifies a growing need for banks to adapt to digital demands.

Digital payments have become integral to modern consumer behavior, experiencing a spike in adoption post-pandemic. McKinsey’s 2023 survey reveals over 90% of consumers now use digital payment methods.

Consumers prioritize convenience, lower costs, and secure interfaces in their payment solutions, pushing fintech providers to innovate continuously. Digital payment features like ease of use, security, and credit score monitoring have become essential for customer satisfaction.

Fintechs are facing stricter regulations as they expand their role in delivering essential financial services. Jurisdictions worldwide are tightening rules to ensure fintech innovations align with financial stability requirements.

Navigating these complex regulations can be challenging for fintechs operating across multiple regions. A strategic partnership with an experienced fintech developer like Leobit can simplify compliance with key standards like GDPR, CCPA, and OWASP.

Generative AI (GenAI) has the potential to add between $200 billion to $340 billion in value to the banking sector. GenAI automates tasks like data entry, fraud detection, credit assessments, and personalized financial advice, revolutionizing operations.

AI-driven fraud detection and tailored customer service can significantly reduce risks and enhance client engagement. However, responsible AI usage remains critical to address concerns around misinformation and bias.

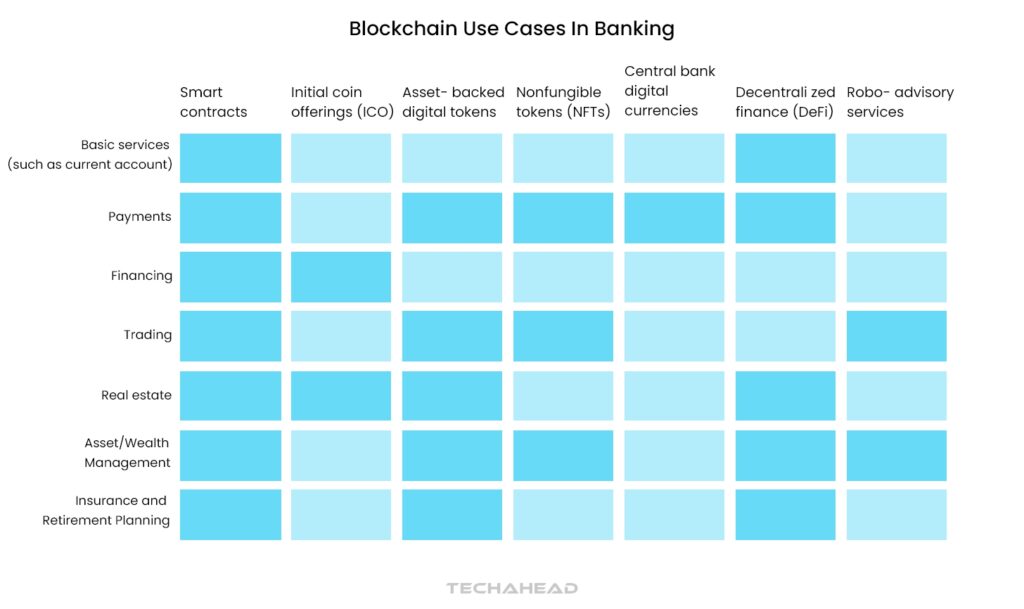

Blockchain technology’s decentralized ledger is revolutionizing banking by enhancing transaction security and transparency. Beyond payments, blockchain’s applications include trade finance, cross-border payments, and smart contracts, streamlining financial operations.

Several countries are exploring Central Bank Digital Currencies (CBDCs) to improve cross-border transaction efficiency, with a few nations already implementing live versions. Blockchain’s ability to facilitate secure, traceable transactions is transforming global finance.

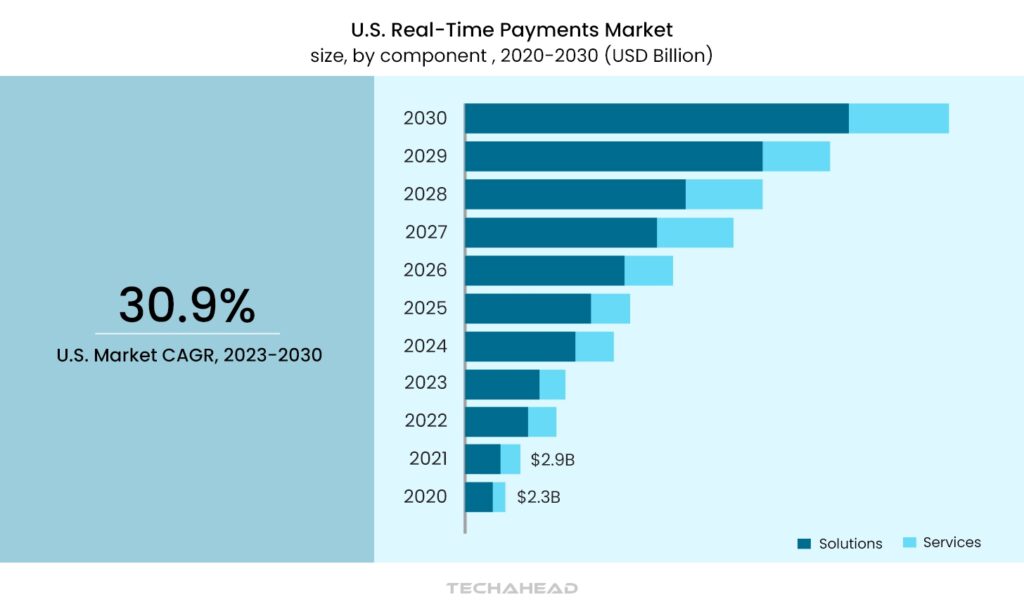

Real-time payments (RTP) are becoming the norm due to the demand for instant settlements and cloud-based transaction solutions. The global RTP market is projected to grow at a rate of 35.5% annually, driven by technological innovations and competitive pressure.

Challenges like legacy infrastructure and fragmentation persist, prompting 77% of financial companies to consider outsourcing RTP capabilities to accelerate implementation.

In 2022, the global real-time payments market was valued at USD 17.57 billion and is projected to expand at a compound annual growth rate (CAGR) of 30.9% from 2023 to 2030.

Personal finance apps have seen massive growth, with users seeking tools beyond basic budgeting to include investment insights. The market is set to rise to $1.57 billion by 2025 as users prioritize apps offering personalized financial advice.

Fintechs can leverage user data from these apps to offer tailored insights, meeting the demand for more personalized financial solutions.

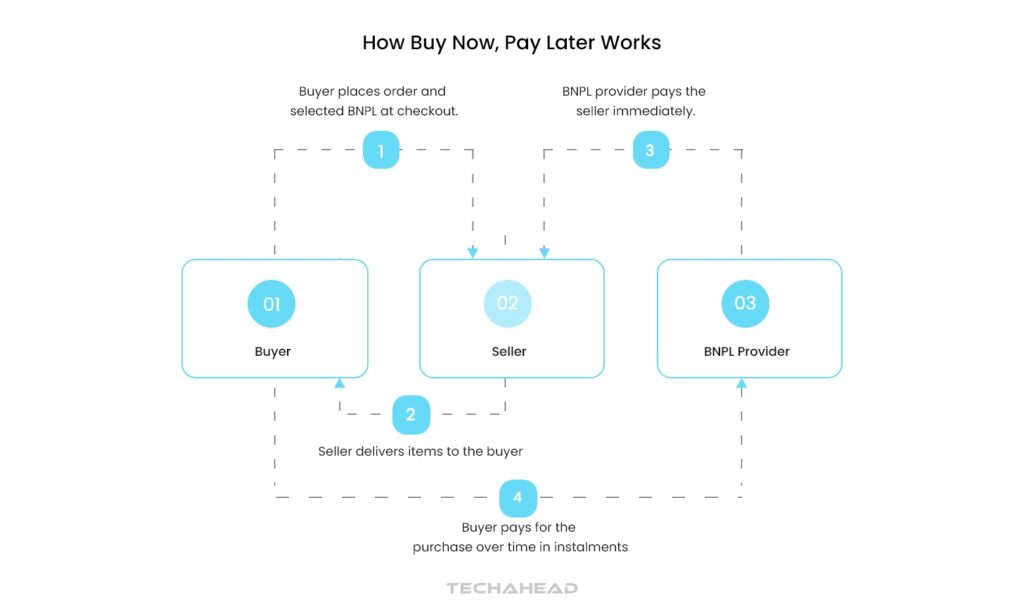

BNPL services offer flexible payment options, rapidly gaining popularity across all age groups.

Banks and fintechs have significant opportunities to tap into this growing market by integrating BNPL into their offerings. However, regulatory scrutiny is intensifying, with new rules expected to ensure responsible lending practices.

In the next decade, there are some technologies that will be the digital transformation within the financial industry. Technological innovation will act as the backbone of fintech, fueling the emergence of disruptive business models.

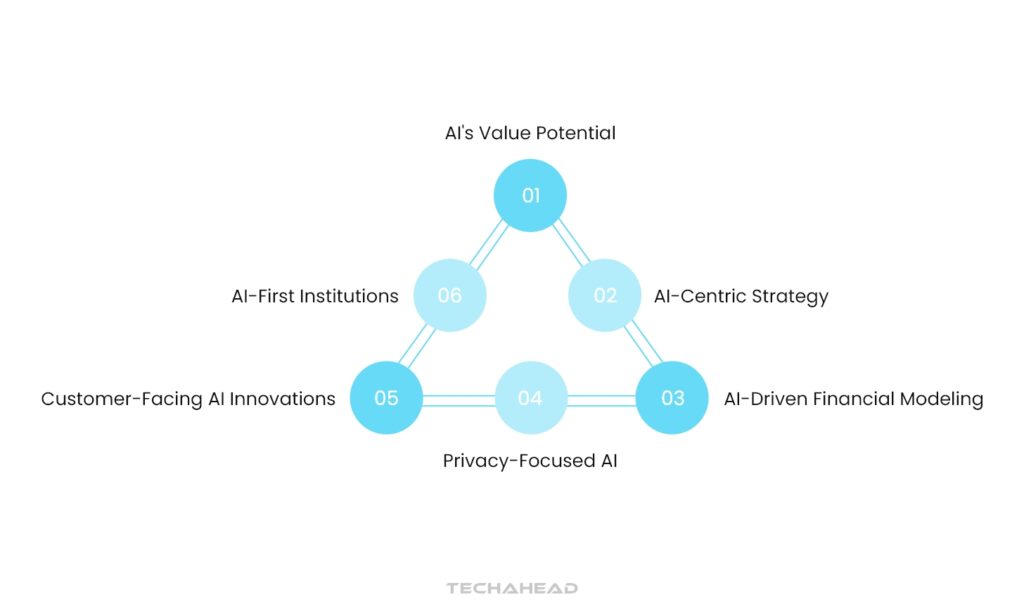

AI is poised to unlock up to $1 trillion in annual value for global banks. Financial institutions will adopt an AI-centric strategy to counter the growing influence of tech giants on their market share. AI’s evolving capabilities will enable financial firms to harness data-driven insights and sharpen their competitive edge.

AI will facilitate automatic factor discovery, identifying key drivers of financial outperformance. This will revolutionize financial modeling, making it more precise and reliable. AI-powered knowledge graphs and graph computing will also play a critical role in analyzing intricate financial networks, revealing hidden patterns by connecting diverse data sources.

Enhanced privacy-centric data analytics will limit data usage to only essential, sanitized information for model training. Techniques like federated learning will boost security by processing data locally instead of centralizing it. Advanced encryption methods, zero-knowledge proofs and secure multi-party computations will set new benchmarks in consumer data protection.

AI’s impact will span across all functions within the financial sector. Customer-facing innovations will include personalized offerings, predictive analytics, AI-driven chatbots, automated trading, and intelligent robo-advisors. On the backend, AI will streamline processes with smarter automation, natural language processing for fraud detection, and improved data handling.

Currently, many banks use AI selectively, focusing on specific tasks. However, industry leaders are now adopting a holistic AI approach across digital operations. This strategy leverages behavioral data to gain insights, driving new opportunities in ecosystem-based financing, where banks partner with non-financial entities to deliver broader customer experiences.

The emergence of “AI-first” institutions will push operational efficiency to new levels, emphasizing extreme automation. By reducing manual tasks and enhancing decision-making through AI diagnostics, banks will optimize performance. AI-first banks will operate with the agility of digital-native companies, launching innovations within days or weeks and integrating seamlessly with external partners for holistic customer solutions.

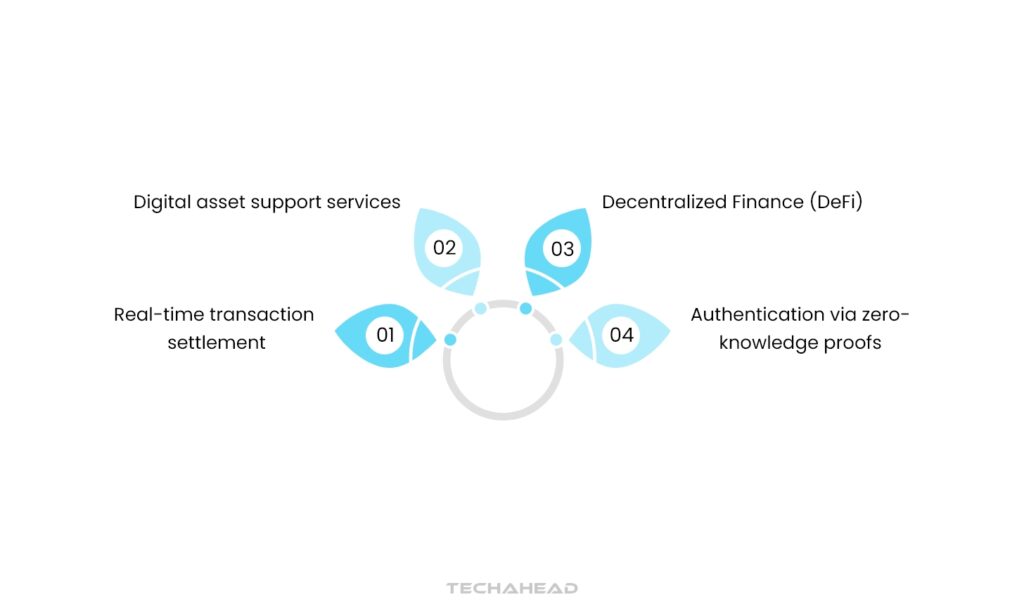

Blockchain and Distributed Ledger Technology (DLT) are set to revolutionize traditional financial frameworks. DLT enables secure, synchronized data sharing across multiple databases, enhancing transparency and efficiency within the financial ecosystem.

DLT systems often leverage blockchain’s cryptographic algorithms to ensure data integrity and immutability across their networks. This technology records, synchronizes, and validates transactions without a central authority, building trust among network participants.

Blockchain’s versatility in supporting ecosystem financing lies in its distributed nature, storing data in multiple locations simultaneously. With cross-chain technology advancing, blockchain interoperability will connect different protocols, streamlining operations across various sectors like payments and supply chain logistics.

Governments are actively exploring blockchain for digital currency and regulatory frameworks. About 60% of central banks are studying Central Bank Digital Currencies (CBDCs), indicating a shift toward digital monetary systems.

Cloud computing will empower financial institutions, unlocking new efficiencies and cost-saving opportunities. By 2030, it’s expected to add over $1 trillion in EBITDA for the top 500 global companies.

Effective cloud migration enhances application development and maintenance efficiency by 38%, cuts infrastructure costs by 29%, and reduces downtime by nearly 57%. This efficiency lowers technical violation costs by 26%, boosting overall productivity and reliability.

Cloud platforms also elevate security through integrated DevOps principles. This approach embeds security throughout development, ensuring a consistent, cross-environmental tech stack, and reducing potential technical risks.

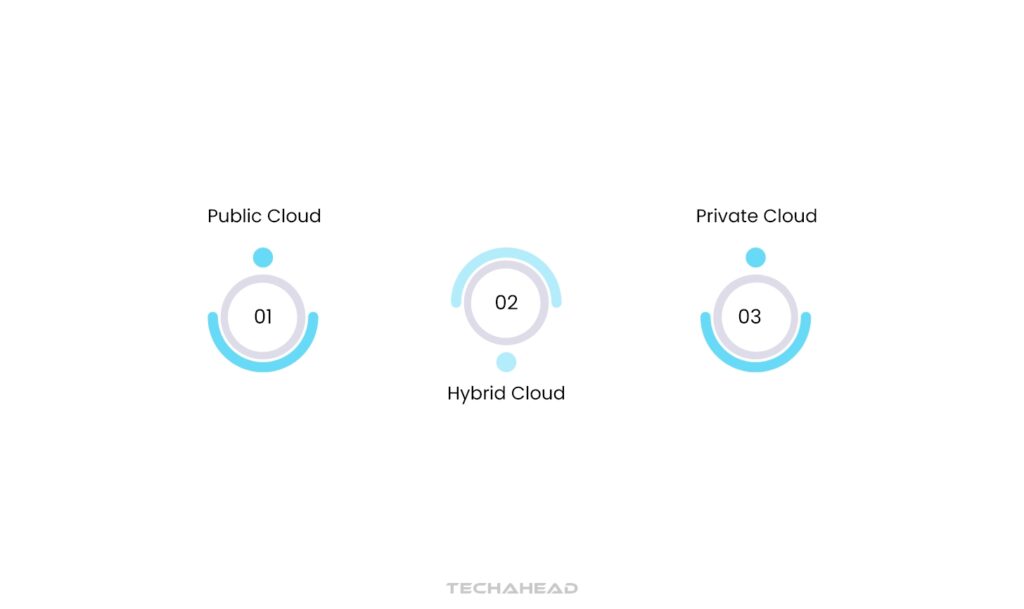

Financial firms should focus on three primary cloud service models: public, hybrid, and private clouds.

Understanding these cloud models enables financial institutions to choose solutions that align with their specific needs and risk appetites.

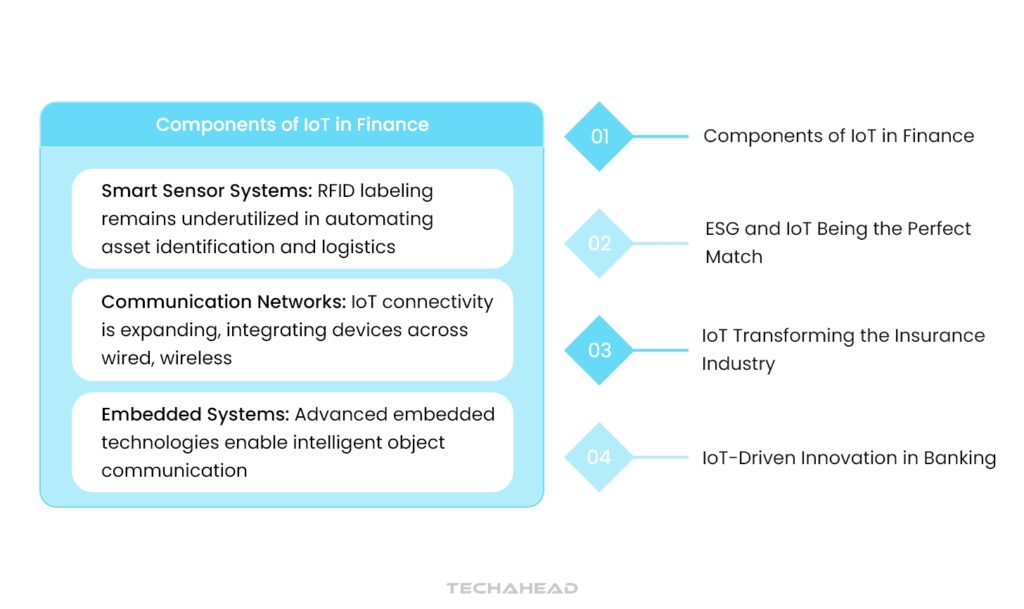

The Internet of Things (IoT) is finally gaining momentum, significantly impacting financial systems. IoT consists of three layers: smart sensor systems, communication networks, and application support.

Environmental, Social, and Governance (ESG) factors now influence investment strategies and regulatory compliance. IoT plays a pivotal role in monitoring energy efficiency, essential to achieving carbon neutrality targets. Carbon trading will increasingly rely on IoT metrics, opening new financial avenues for proactive businesses.

IoT is reshaping insuretech by enabling precise risk assessment and streamlined processes. Auto insurers traditionally used general data like age and location to set premiums. Now, real-time data on driving behavior directly informs risk profiles, allowing for more tailored policy pricing.

Frequent customer interactions facilitated by IoT enhance engagement, enabling insurers to provide value-added services. This shift transforms the insurer’s role from a passive service provider to an active participant in customer journeys, improving loyalty and satisfaction.

IoT is refining risk management in banking through enhanced transparency in inventory and property financing. Integrating IoT with blockchain ensures that financial records align with real-world transactions, creating a robust trust ecosystem.

In logistics, IoT revolutionizes trade finance by enabling precise tracking of goods flow. This transparency allows banks to innovate with products like on-demand liquidity and services powered by smart contracts, reducing transaction times.

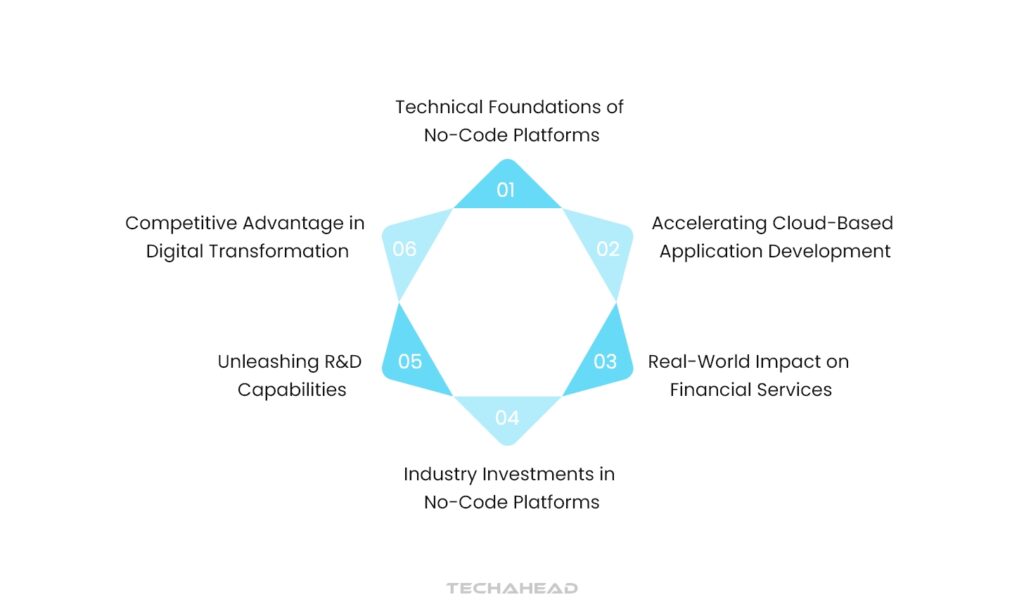

Current digital economy is speeding and scaling vital for new businesses striving to gain a competitive edge. Open-source software, serverless architectures, and SaaS solutions have become essential for both technology startups and traditional financial institutions in the Fintech space.

No-code development platforms (NCDPs) and low-code platforms enable both developers and non-technical users to build applications effortlessly. These platforms utilize intuitive graphical user interfaces, like drag-and-drop features, reducing reliance on traditional coding.

Organizations utilize NCDPs to speed up cloud application development while synchronizing technology with evolving business strategies. Automated workflows, like audit trails and document generation, ensure seamless compliance in regulated sectors.

For financial institutions, these platforms enable agile responses to dynamic market conditions, improving time-to-market for solutions. This capability is invaluable in sectors where speed and compliance are critical for maintaining a competitive edge.

Tech giants are heavily investing in these innovations. Google Cloud’s acquisition of AppSheet and investment in Unqork highlight the growing reliance on low-code and no-code technologies.

No-code/low-code platforms liberate research and development resources, allowing institutions to manage multiple projects simultaneously. This flexibility equips traditional financial firms to match the innovation pace of fintech startups.

These platforms provide the scalability needed for enterprise-level digital transformation, bridging the gap between traditional finance and agile fintech disruptors.

The financial sector is undergoing a transformative shift, driven by advancements in fintech. Fintech innovations are not only redefining convenience and accessibility in financial services but also setting new standards. Like for personalized experiences and efficient operations.

By embracing emerging technologies like Generative AI, cloud computing, and blockchain, financial institutions can unlock new opportunities. The future of the finance industry lies in a seamless blend of technology-driven innovation and customer-centric strategies. With fintech leading the way in shaping a more connected, efficient, and secure financial landscape.

AI is revolutionizing the finance industry by enhancing customer service through chatbots, automating routine tasks, detecting fraud, and offering personalized financial advice. It also enables predictive analytics to better understand customer behavior and optimize decision-making processes.

Blockchain technology is reshaping banking by providing secure, transparent, and efficient transaction processes. It supports applications such as cross-border payments, trade finance, and smart contracts, making financial operations more streamlined and trustworthy.

Digital-only banks, or neobanks, offer a fully online banking experience, which appeals to consumers seeking convenience, lower fees, and competitive interest rates. Their rise is fueled by the demand for fast, mobile-based financial solutions, particularly among younger generations.

Cloud computing drives significant improvements in cost efficiency, scalability, and data security for financial institutions. By adopting cloud solutions, banks can enhance their application development, reduce infrastructure costs, and maintain high standards of data protection.

IoT is enhancing financial services by enabling real-time data tracking and more accurate risk assessments. It supports better inventory management in supply chains, facilitates personalized insurance products, and helps banks develop innovative financial solutions through connected devices.

We use cookies to ensure our website functions properly, improve performance, and provide a personalized experience. You can choose which types of cookies to allow below.

Required for core functionality such as security, network management, and accessibility. These cannot be disabled.

Help us understand site traffic and user interactions so we can improve performance and usability.

Enable enhanced functionality and personalization such as language or region preferences.

Used to deliver relevant ads, track campaign performance, and measure advertising effectiveness.