Staff Augmentation

Access top-tier talent on demand: Dedicated, Hourly, or Flexible.

Copy Link

Copy Link Share on X

Share on X Share on Facebook

Share on Facebook Share on LinkedIn

Share on LinkedIn

Sending international business payments often means bleeding cash in transaction fees. While the total cross-border payment flows exceeded $200 trillion in 2025, the main challenge remains: traditional banks charge 3-8% per transaction and require 3-5 days for settlement.

However, when Satoshi Nakamoto launched Bitcoin on January 3, 2009, embedding the message “Chancellor on brink of second bailout for banks” in the genesis block, it was not just creating a cryptocurrency; it was declaring war on the entire legacy financial system. That peer-to-peer system eliminated the need for central banks and intermediaries.

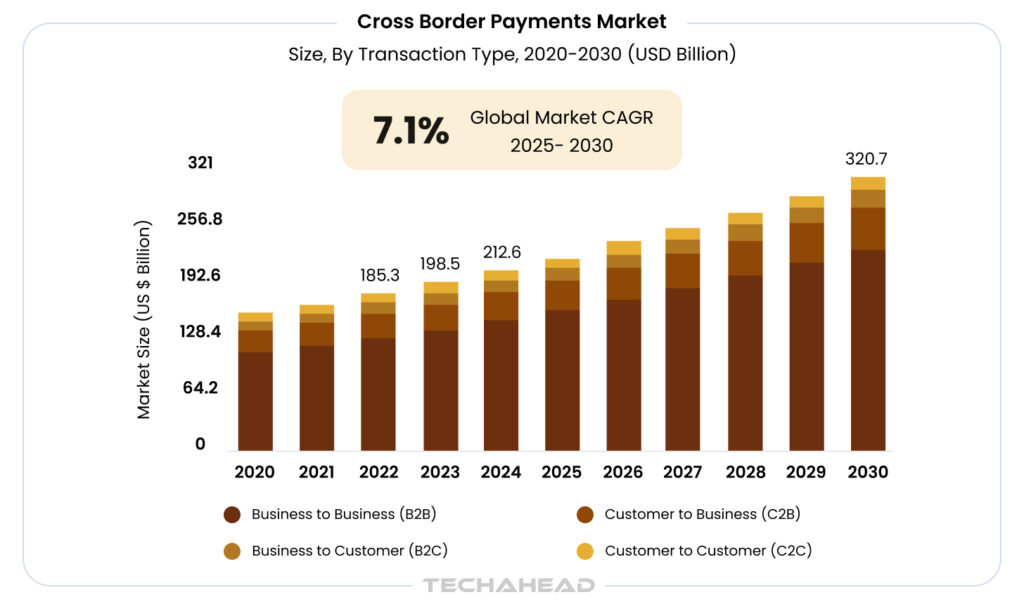

Today, the cross-border payments revenue market is projected to reach $320 billion by 2030, and blockchain technology is revolutionizing how enterprises move money globally. Companies like JPMorgan’s Kinexys now process billions of dollars daily through blockchain rails, while others achieve instant settlements that once took days. The blockchain ecosystem has reshaped the global financial ecosystem. If you rely on traditional banks or want to build a blockchain-based platform, this guide explores everything you need to know before investing in 2025. So let’s dive in:

Key Takeaways

- Blockchain enables instant cross-border settlements, helping you avoid traditional 3-5 day processing delays.

- Every blockchain transaction is cryptographically secured and nearly impossible to tamper with.

- Automated smart contracts eliminate manual intervention, releasing payments as soon as conditions are met.

- Stablecoins enable global transactions 24/7, removing delays from FX conversion and banking hours.

- Liquidity pool arbitrage gives you better exchange rates than traditional banking routes.

What are the Challenges with Traditional Cross-Border Payments?

According to Grand View Research, the global cross-border payments market size was estimated at USD 212.55 billion in 2024 and is projected to reach USD 320.73 billion by 2030.

However, every international wire transfer costs your enterprise thousands in hidden fees, days in processing delays, and the blockchain-based financial ecosystem is ready to address these challenges with more flexibility and security. First, let’s understand the challenges of traditional cross-border payments:

The High Cost of Moving Money Globally

If you are running an enterprise that operates internationally, you have likely felt the sting of traditional cross-border payment fees. Banks and intermediaries usually charge anywhere from 3-8% per transaction. It means when you are sending millions across borders regularly, these costs add up fast.

Waiting Days for What Should Take Minutes

Another challenge is long waiting times. For example, your suppliers need payment, but your traditional wire transfer sits in processing limbo for 3-5 business days. Legacy banking systems need multiple intermediary banks to verify and process international transactions. That creates unnecessary delays, but you can improve this cash flow management with the blockchain ecosystem.

Operating in a Black Box

With traditional payments, you send money and hope for the best. You cannot track where your payment is in real-time. So this lack of transparency, which could be solved by professional data analytics services, makes financial planning nearly impossible. Sometimes, it leaves you answering frustrated calls from partners wondering where their payment is.

How Blockchain and Web 3.0 Change the Game?

Blockchain technology eliminates these pain points with direct, peer-to-peer transactions that bypass traditional intermediaries. With smart contracts and decentralized networks, you can send payments that settle in minutes rather than days. Moreover, the process is completely transparent and fees are as low as a few dollars.

The real question becomes: how does blockchain technology actually deliver on these promises? The answer lies in architecture.

How Blockchain Works in Cross-Border Transactions

Blockchain technology is revolutionizing the way cross-border payments are conducted in a decentralized and transparent way.

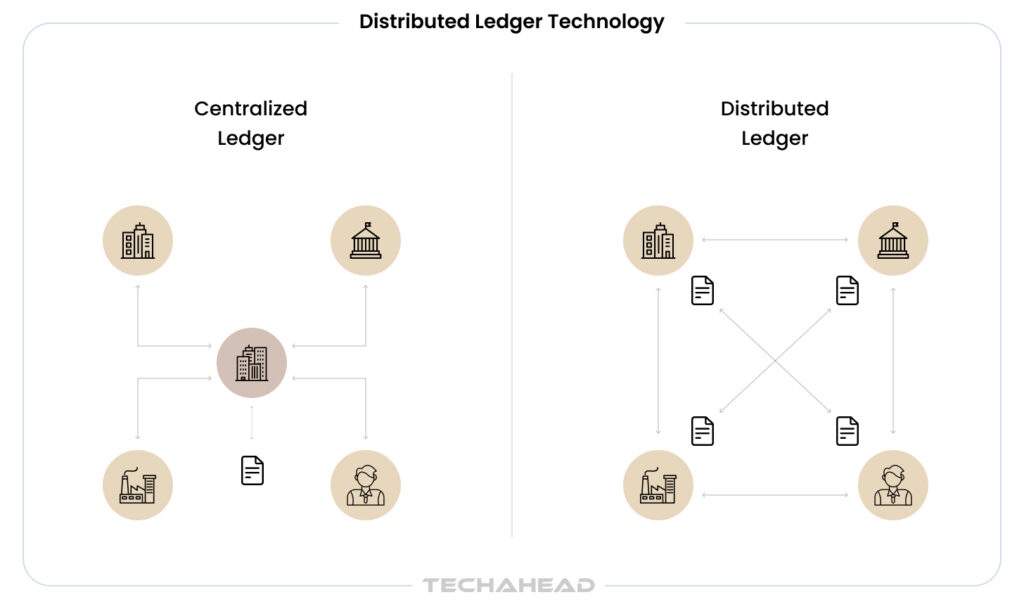

Distributed Ledger Technology (DLT)

At the core of blockchain cross-border payments is Distributed Ledger Technology (DLT). Unlike traditional centralized payment systems, DLT operates on a network of nodes (computers) that maintain synchronized and up-to-date copies of the payment ledger.

Here, each transaction is recorded in a block of data, which is cryptographically linked to prior blocks. This distributed approach eliminates the need for intermediaries (banks and other institutions), which reduces the delays.

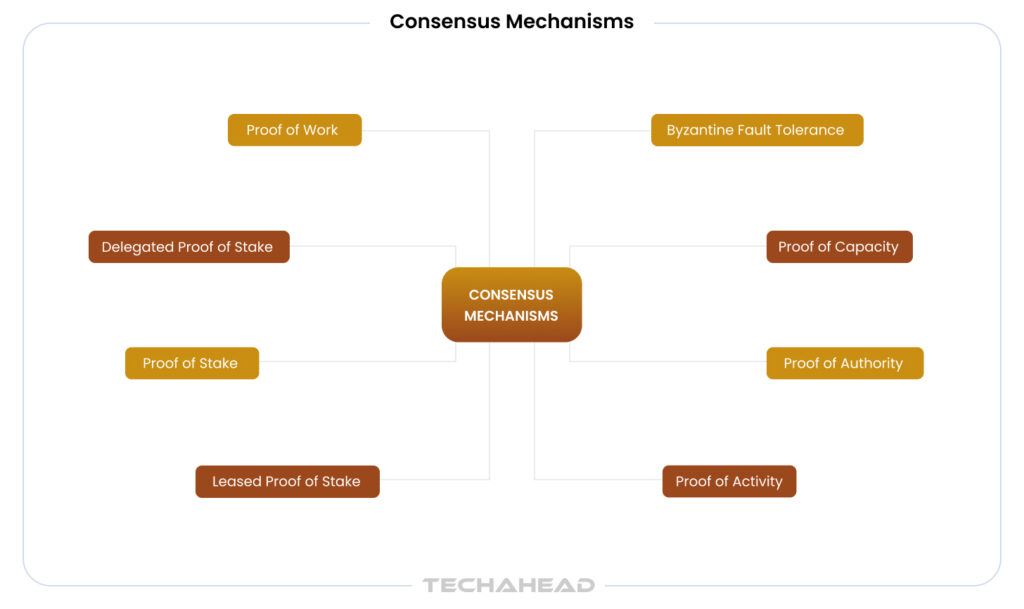

Consensus Validation

Consensus protocol is another important part that validates transactions. These are predefined rules that nodes follow to verify transaction legitimacy. It acts as the security backbone for blockchain transactions.

Multiple validator nodes must agree on each transaction’s legitimacy using cryptographic algorithms like Proof-of-Stake or Byzantine Fault Tolerance. Each transaction receives a unique cryptographic hash that makes tampering impossible. When majority nodes validate a transaction, it achieves “finality”. This distributed validation process eliminates the single points of failure found in traditional banking systems, which means your payments are secure without relying on central authorities.

Smart Contracts

Another important part is the smart contracts; these are programmable contracts embedded directly on the blockchain. They automate payment workflows without human intervention. For example, releasing funds automatically once goods are delivered or services are confirmed. Such automations reduce the risk of errors and streamline currency conversion processes.

Now that you understand blockchain’s technical foundation, let’s explore the specific enterprise benefits this technology delivers.

How Blockchain Connects and Works with Existing Payment Methods?

Have you ever wondered how banks make use of blockchain development services and integrate or connect them into their existing payment models? To understand this, you only need to know about three key components:

The Global Language (ISO 20022)

SWIFT is the existing platform that allows cross-border payments, and for blockchain to be a success, it must be able to communicate with it. Modern blockchain platforms now structure data in this standardized, rich XML format to talk to old frameworks. This allows crypto transactions to carry detailed remittance data, like invoice numbers and tax IDs. These details are directly sent to the receiver’s traditional bank account without being rejected.

Layer 2 Scaling (The Speed Layer)

Why pay $50 in gas fees when you can pay $0.01? Enterprises have stopped transacting directly on slow “mainnets” (Layer 1) like Ethereum. Instead, we now use Layer 2 “Rollups.” These networks bundle thousands of transfers off-chain and process them instantly, only writing the final result back to the main blockchain. This is how platforms now achieve VISA-level transaction throughput without crashing the network.

Cross-Chain Interoperability (CCIP)

A cross-platform payment mechanism should be able to connect, send, or receive money for any bank, public or private, from the same or different countries. However, Blockchain’s core functionality doesn’t align with cross-platform guidelines. The launch of Cross-Chain Interoperability Protocols (CCIP) allows you to securely teleport tokens and messages between these blockchains. It creates a “network of networks,” ensuring you can do transactions with anyone.

Key Benefits of Blockchain for Enterprises for Cross-Border Payments

Enterprise blockchain adoption accelerates when technical capabilities align with business objectives. The following benefits show why industry leaders are abandoning traditional payment infrastructure and choosing blockchain-based ecosystems.

Atomic Settlement and DVP Mechanisms

Blockchain allows true delivery-versus-payment (DVP) execution through advanced Cross-Chain Interoperability Protocols (CCIP). Enterprises can now eliminate Herstatt risk entirely across different networks. Modern smart contracts provide cryptographic guarantees that either both parties receive their respective assets or the transaction reverts completely. It means this atomic swapping technology eliminates counterparty settlement risk without needing a trusted third party.

Liquidity Pool Arbitrage and Dynamic Routing

Decentralized liquidity pools allow enterprises to access global liquidity across multiple AMMs and DEXs. Next-generation aggregators automatically identify optimal paths through Uniswap v4, Curve, and Balancer to maximize execution efficiency. This capability provides enterprises with better exchange rates compared to traditional FX markets by splitting large orders across the most liquid pools.

Regulatory Compliance Through Programmable Money

Zero-Knowledge Proof (ZKP) technology now allows automatic adherence to jurisdiction-specific regulations during cross-border transfers. Smart contracts embed zk-KYC (Zero-Knowledge Know Your Customer) checks, sanctions screening, and reporting requirements directly into payment rails. This programmable compliance reduces manual oversight costs and protects user privacy to evolve regulatory frameworks globally without requiring system upgrades.

MEV Protection and Transaction Privacy

Enterprise payments benefit from MEV-resistant transaction ordering through private RPC endpoints and commit-reveal schemes. Solutions like Flashbots Protect prevent front-running of large cross-border transactions, while zk-SNARKs allow selective disclosure of payment details to regulatory authorities without exposing sensitive commercial information to competitors.

Moving from technical possibilities to practical implementation, the evidence comes from established enterprises that have transformed their payment operations with blockchain solutions.

TL;DR section: Real-World Use Cases and Success Stories

| Company | Use Case | Key Benefit |

|---|---|---|

| JPMorgan Chase | Kinexys platform for 24/7 cross-border payments | Real-time global transfers, no weekend downtime |

| Santander | Ripple-powered One Pay FX | 2-second international transfers vs 3 days |

| American Express | Ripple-based US–UK payment corridor | End-to-end visibility, faster cross-border payments |

| Walmart | Blockchain supplier payments | Instant supplier payouts, 60% cost reduction |

| Mercedes-Benz | Blockchain supply chain financing | Instant supplier payments, improved cash flow |

Real-World Use Cases and Success Stories

Industry leaders risk reputations on blockchain implementations because ‘results speak louder than promises’. These enterprise success stories have the advantages of driving widespread blockchain payment adoption across industries.

JPMorgan Chase

Remember when JPMorgan’s CEO called Bitcoin a “fraud”? Well, the bank has certainly changed its tune. Their Kinexys Digital Payments platform now allows 24/7 cross-border transfers in near real-time across borders. It has been processing over $2 billion in daily transactions. Instead of waiting 3-5 days for traditional correspondent banking, they transfer funds (for enterprise clients) instantly between accounts globally. The real game-changer? They have eliminated the weekend downtime, and you can transfer funds 24/7/365 with only a brief 3-hour maintenance window on Saturdays.

Santander

Santander partnered with Ripple for cross-border payment processing. While traditional banks take a 3-day settlement period, Santander offers the transfer in 2 seconds. Their One Pay FX service, launched in 2018, transformed how the $80 billion banking giant handles international transfers. It reduces the uncertainty for their corporate clients, especially in cash flow management.

American Express

Moreover, AmEx partnered with Ripple to create direct payment corridors between the US and UK. It initially allows customers to connect traceable cross-border non-card payments to UK Santander bank accounts. Besides that, their blockchain solution provides end-to-end transaction visibility, something that was impossible with traditional SWIFT messaging.

Walmart

Walmart revolutionized its supplier payment system with the blockchain ecosystem. Instead of waiting weeks for payment reconciliation after delivery verification, suppliers now receive automatic payments the moment goods are verified and recorded on their blockchain system. This eliminated payment disputes and improved supplier relationships while reducing Walmart’s accounts payable processing costs by 60%.

Mercedes-Benz

Mercedes-Benz implemented blockchain-based supply chain financing for its tier-2 and tier-3 suppliers. Their system automatically releases payments to component manufacturers the moment parts are verified at assembly plants. As a result, it eliminates the traditional 90-day payment cycles that strained smaller suppliers’ cash flow. Such use of blockchain solutions improves supplier loyalty across their global manufacturing network.

So, current blockchain implementations prove the technology works, but emerging trends reveal how payment systems will evolve in the coming years.

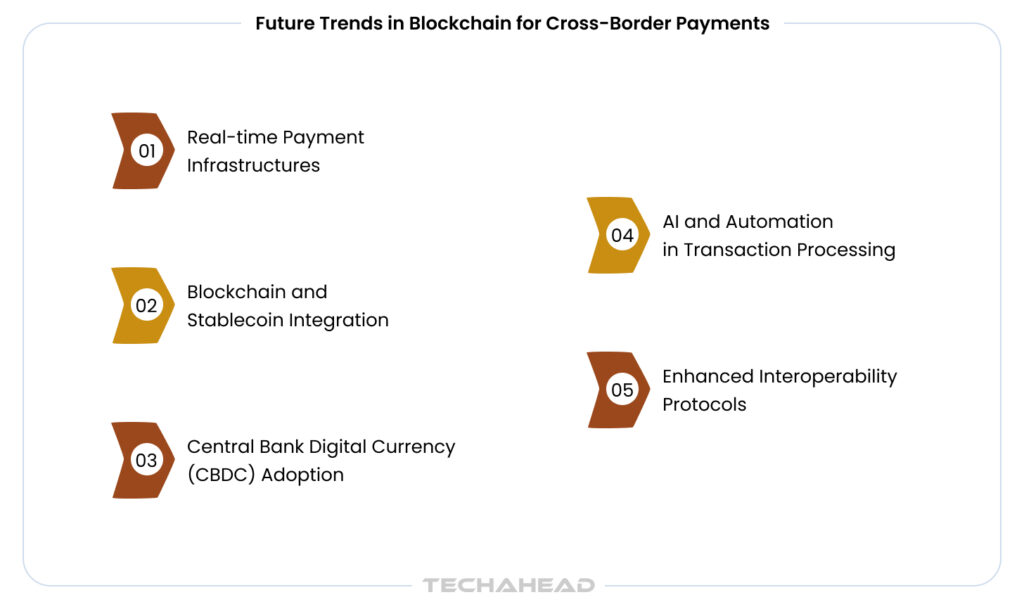

What are the Future Trends in Blockchain for Cross-Border Payments?

Today’s blockchain payments are tomorrow’s legacy systems. Enterprise blockchain adoption will accelerate as emerging technologies eliminate remaining limitations. These trends represent the future of international commerce and global payment infrastructure.

Real-time Payment Infrastructures

Next-gen blockchain platforms are ready to offer 24/7 real-time settlement of cross-border transactions. Decentralized ledgers reduce latency drastically compared to legacy banking. Supported by expert cloud consulting services, such platforms provide enterprises with access to instant liquidity that improves cash flow and operational efficiency. As a result, you can expect frictionless payments across borders without dependency on intermediaries.

Blockchain and Stablecoin Integration

Stablecoins, digital assets pegged to fiat currencies, act as programmable rails on blockchain networks. Enterprises integrate stablecoins with blockchain to bypass slow correspondent banking. Overall, it improves transparency for scalable global commerce.

Central Bank Digital Currency (CBDC) Adoption

CBDCs are sovereign digital currencies issued on blockchain or distributed ledgers. Increasing adoption by central banks offers enterprises secure payment options with reduced counterparty risks. CBDCs promise enhanced liquidity and programmable smart contracts integration that transform traditional international payments with state-backed digital money.

AI and Automation in Transaction Processing

Artificial intelligence development and robotic process automation optimize blockchain cross-border payments via intelligent fraud detection. AI-driven platforms enhance transaction accuracy, reduce human errors, and accelerate processing at scale. It means, as an enterprise owner, you can expect faster, cost-effective global payments.

Enhanced Interoperability Protocols

New interoperability standards mean seamless interaction across multiple blockchain networks. Enterprises benefit from

- cross-chain atomic swaps

- token wrapping

- standardized messaging

- enhanced protocols

- reduced latency

Overall, advanced interoperability protocols help to expand the reach of the DeFi ecosystem.

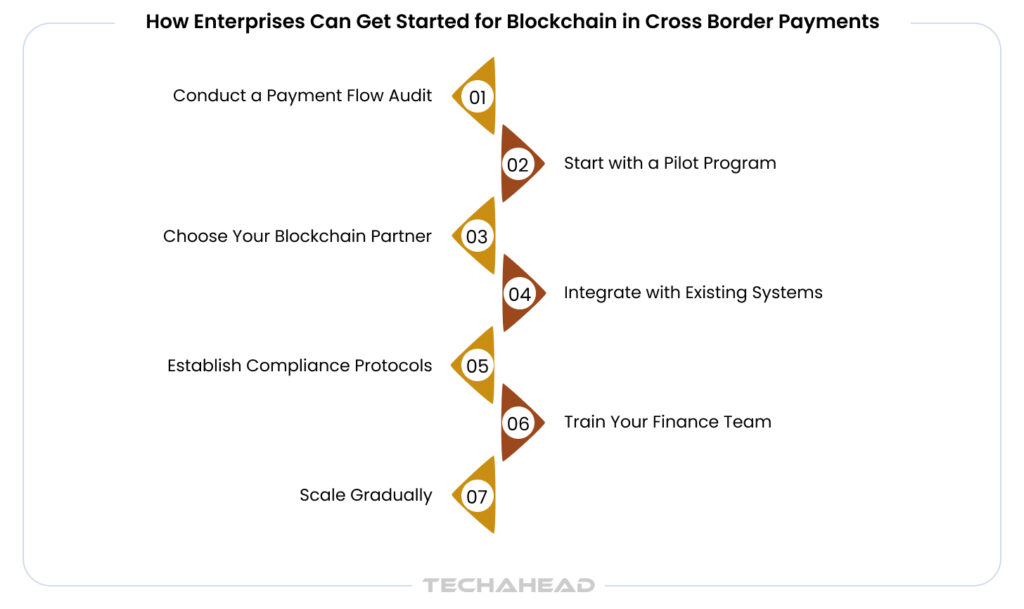

How Enterprises Can Get Started with Blockchain in Cross-Border Payments

Getting started with blockchain-powered cross-border payments does not require a huge investment or advanced financial infrastructure. It needs strategic steps and a phased approach for measurable results. Here is the step-by-step implementation process:

Conduct a Payment Flow Audit

Map your current cross-border payment processes and identify pain points like high fees and settlement delays. Quantify exactly how much capital is trapped in pre-funded nostro accounts.

Start with a Pilot Program

Select low-risk, high-frequency payment corridors (such as monthly contractor payouts) to test stablecoin settlements. Use liquid pairs like USDC or EURC to ensure easy off-ramping at the destination.

Choose Your Blockchain Partner

Consult with a blockchain app development company to choose the best blockchain platforms that support ISO 20022 messaging standards. Making the right choice here ensures a long-term enterprise app development benefits, as a partner who prioritizes cross-chain compatibility (CCIP) ensures you aren’t locked into a single network.

Integrate with Existing Systems

Next, your blockchain solution must connect seamlessly with your current ERP, accounting, and treasury management systems. Modern solutions use API-first middleware to translate on-chain events into standard accounting entries your finance team understands.

Establish Compliance Protocols

Work with legal teams to meet all regulatory requirements.

Train Your Finance Team

Provide training on blockchain payment monitoring and troubleshooting procedures. Your finance team must know how to approve transactions related to blockchain.

Scale Gradually

Now, time to expand to additional payment corridors and higher transaction volumes once your pilot demonstrates consistent results.

Remember that, in the blockchain industry, the most successful projects start small and scale systematically when the solution proves valuable for the target audience.

Conclusion

The technology has matured beyond experimental phases that eliminate traditional pain points with better transparency and control. However, success depends on partnering with the right blockchain development company that understands both blockchain intricacies and enterprise requirements. At TechAhead, our developers combine deep blockchain expertise with proven enterprise development experience. Contact us today to discuss how our blockchain solutions accelerate your business growth.

Which blockchain platforms work best for enterprise payments?

Ethereum dominates with robust smart contract capabilities, while Ripple excels in banking partnerships. Hyperledger Fabric offers private networks, and Polygon provides cost-effective scaling for high-volume enterprise payment operations.

Is blockchain secure for large international transactions?

Yes, blockchain uses cryptographic security and immutable ledgers. Enterprise-grade platforms like JPMorgan’s Kinexys process billions daily with military-grade encryption, multi-signature protocols, and comprehensive audit trails for security.

Can blockchain payments integrate with existing ERP systems?

Absolutely. Modern blockchain platforms offer REST APIs, webhooks, and middleware solutions that seamlessly connect with SAP, Oracle, and other ERP systems without requiring complete infrastructure overhauls.

What happens if blockchain payment transactions fail?

Failed transactions are automatically reverted through smart contract logic. Funds return to sender wallets immediately, and detailed error logs help identify issues. No money is lost in properly designed blockchain systems.

Are blockchain payments reversible like traditional wire transfers?

No, blockchain transactions are immutable once confirmed. However, smart contracts can include escrow mechanisms, dispute resolution protocols, and conditional releases to provide similar protection through programmable safeguards.