Staff Augmentation

Access top-tier talent on demand: Dedicated, Hourly, or Flexible.

Copy Link

Copy Link Share on X

Share on X Share on Facebook

Share on Facebook Share on LinkedIn

Share on LinkedIn

Peer-to-peer investment platforms are digital marketplaces that directly connect investors with borrowers. While traditional banks approve only 27% of small business loan applications, peer-to-peer platforms are bridging this $5.2 trillion global credit gap that conventional lenders leave behind.

You are probably familiar with the frustrations of traditional financing. Banks take 30-90 days for loan approvals, charge average interest rates of 6-13% and reject 73% of applications. On the other hand, Venture capital firms fund less than 1% of startups they review; they focus more on high-growth tech companies but usually ignore established businesses struggling for growth capital. Alternative options like merchant cash advances carry effective annual rates exceeding 40%.

Peer-to-peer investment platforms change this equation entirely. Instead of banks acting as expensive middlemen, these platforms directly connect investors seeking returns with businesses needing capital. The result? Win-win for both: investors earn 5-12% annual returns and borrowers access funds in days rather than months, often at more competitive rates than traditional banks offer.

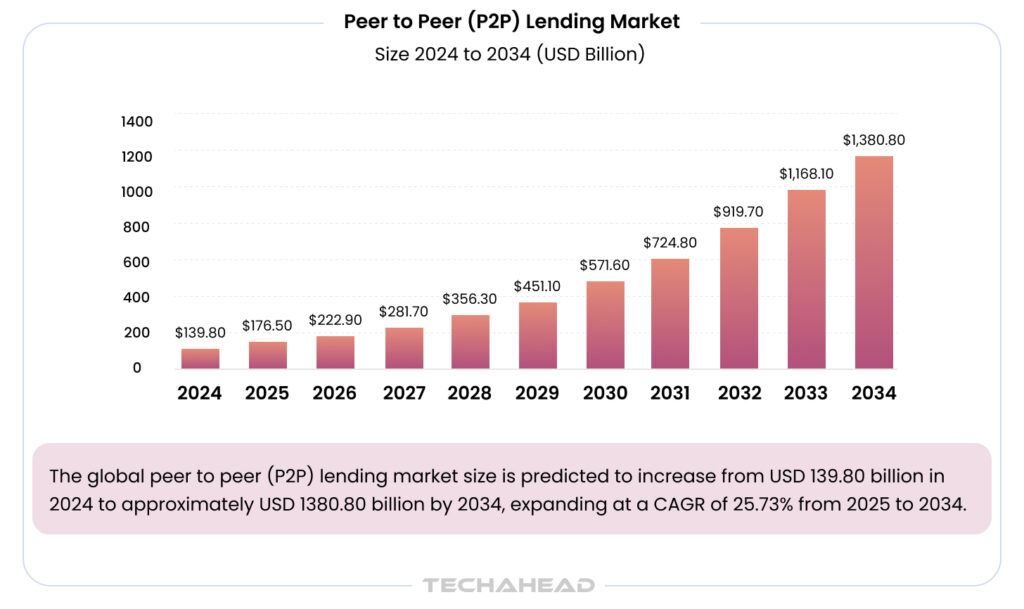

Due to its several benefits, P2P lending volume reached $150 billion globally in 2023, with projections showing the market hitting $558 billion by 2027, a compound annual growth rate of 29.7%.

In China alone, P2P platforms processed over $200 billion in transactions before regulatory changes. The UAE, United States and Europe are now experiencing similar exponential growth, that is why in today’s blog, we are going to explore the future of the P2P investment platform and how you can build your platform for global expansion. Let’s dive in:

Key Takeaways

- P2P platforms bridge the $5.2 trillion credit gap that offers faster, accessible loans

- AI credit scoring improves approval rates and reduces defaults by 75%.

- Successful P2P platforms must focus on user experience with seamless onboarding and responsive interfaces for borrowers and investors alike.

- Automation for KYC, AML, and data privacy prevents penalties and builds trust among users.

- Smart contracts and DeFi protocols reduce operational costs by 60%.

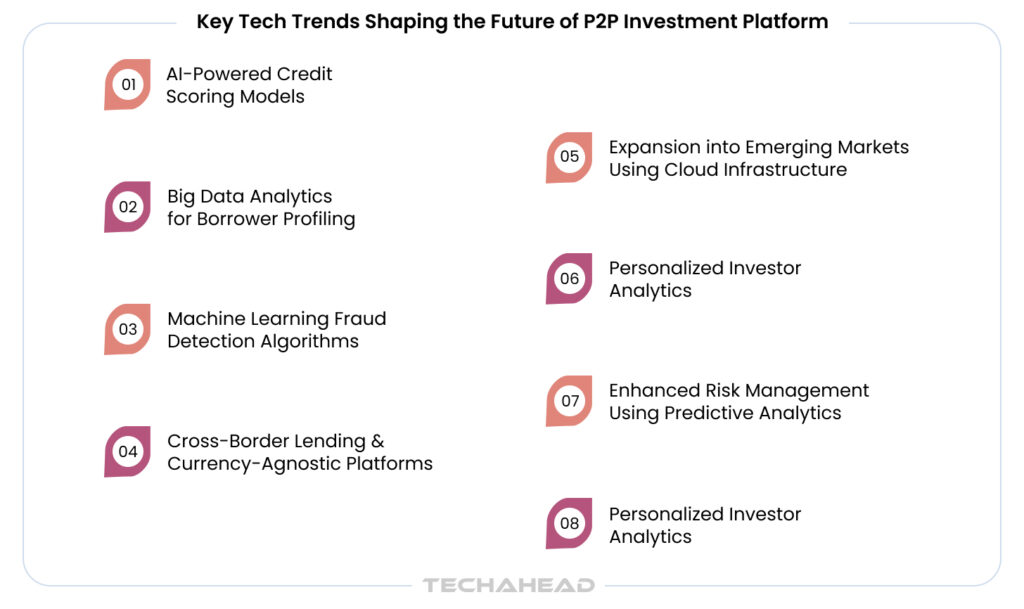

Key Tech Trends Shaping the Future of P2P Investment Platform

Technology is transforming P2P investment platforms from simple matching services into secure financial ecosystems. According to the Precedence Research, the global peer to peer (P2P) lending market size was estimated at USD 139.8 billion in 2024 and is predicted to increase from USD 176.5 billion in 2025 to approximately USD 1,380.80 billion by 2034, expanding at a CAGR of 25.73% from 2025 to 2034.

Here are the tech trends that reshape how platforms assess risk, detect fraud, and maximize returns for investors:

AI-Powered Credit Scoring Models

Today’s AI-powered models analyze over 10,000 data points in real-time. Companies like Upstart have seen 75% fewer defaults by using these advanced algorithms. What does this mean for you?

- Better loan approval rates

- Reduced risk

- Higher returns

AI-powered models predict creditworthiness with 40% more accuracy than traditional methods. It turns previously “unbankable” borrowers into profitable opportunities for your investment portfolio.

Big Data Analytics for Borrower Profiling

Modern P2P platforms process different data sources per application, which creates detailed, ‘trustworthy’ borrower profiles. Research shows that platforms using data analytics features for borrower profiling experience 30% lower default rates. It means you can make informed investment decisions based on multi-dimensional borrower profiles rather than just basic financial statements.

Machine Learning Fraud Detection Algorithms

Did you know that in 2024, fraud attempts in online lending increased by 52%? However, here is the good news: advanced machine learning algorithms now catch 99.5% of fraudulent applications before they reach your investment dashboard. These systems learn from millions of transactions that identify suspicious patterns in milliseconds. For you, your capital is protected by technology that gets smarter every day. It reduces fraud losses to ‘virtually’ zero and maintains the integrity of your investment returns.

Cross-Border Lending & Currency-Agnostic Platforms

Now, you do not need to rely only on domestic opportunities; you can invest globally with blockchain and cloud P2P platforms. The advantage of new blockchain-based platforms is that they allow you to lend in multiple currencies without worrying about exchange rate fluctuations.

For example, you could be funding a small business in Kenya while sitting in New York with Bitcoin or Ethereum. That is why the cross-border P2P lending market is projected to grow 23% annually through 2027, that gives you access to higher-yield opportunities in emerging economies.

Read More,

How Automated Financial Reporting Transforms Modern Finance Teams?

10 Ways Workplace AI and Automation Are Boosting Productivity for Enterprises

Expansion into Emerging Markets Using Cloud Infrastructure

Emerging markets represent 85% of the world’s unbanked population; that is your untapped opportunity! Cloud infrastructure now costs 70% less than traditional banking systems and it allows your P2P platforms to expand into markets like Southeast Asia and Africa.

For you, it means access to borrowers willing to pay 15-25% interest rates due to limited local financing options. Companies like Tala have already disbursed over $2 billion in microloans using cloud-first approaches.

Personalized Investor Analytics

Modern platforms use AI to create personalized analytics that match your risk tolerance. Instead of generic market data, you get tailored insights showing which loan categories perform best for investors with your profile. These smart dashboards predict optimal portfolio allocation and send alerts when opportunities match your criteria. It helps you achieve 20-30% better returns through data-driven decision making.

Enhanced Risk Management Using Predictive Analytics

Predictive analytics has revolutionized risk management, such platforms now forecast potential defaults 6-12 months in advance. You can analyze different economic indicators, such as borrower behavior changes, market trends, to avoid losses before they happen.

Studies show that platforms using advanced predictive models reduce investor losses by up to 45%. It means you can confidently diversify your portfolio knowing that advanced algorithms are continuously monitoring and protecting your investments against emerging risks.

These technological advances are transforming P2P platforms. So, whether you are evaluating your existing platforms or building new ones, you need a strategic approach for launching a successful P2P investment platform for your target audience.

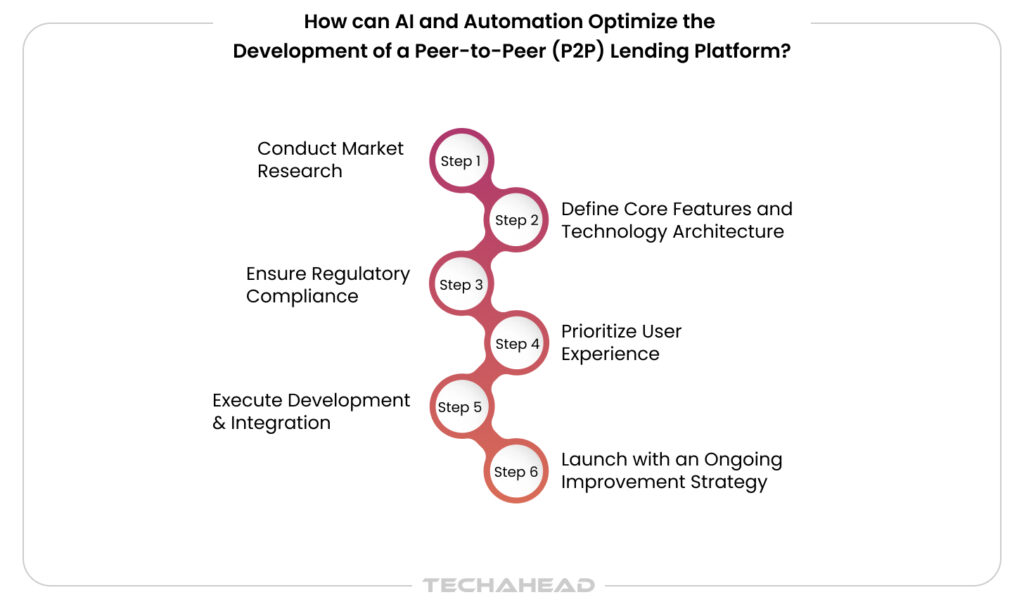

How can AI and Automation Optimize the Development of a Peer-to-Peer (P2P) Lending Platform?

With these powerful technologies reshaping the industry, the question becomes: how do you find the right approach to utilize these innovations effectively? Here is your step-by-step guide:

Step 1: Conduct Market Research

The first step is conducting deep market research. It is essential to understand the needs of both borrowers and investors. You need to identify gaps within existing solutions. This insight ensures that your P2P platform addresses genuine market demands and positions itself effectively against competitors.

Step 2: Define Core Features and Technology Architecture

Next, clearly define the platform’s essential features. Here you need to consider advanced technologies such as AI-driven credit scoring, blockchain for transaction transparency or automated risk management tools for better scalability/security. Besides that, consult with a fintech app development service partner to select advanced technology stack for long-term sustainability.

Step 3: Ensure Regulatory Compliance

The most important part is the adherence to applicable financial regulations (including KYC, AML, and data privacy). Developing a risk management framework helps you navigate fraud detection, loan default mitigation that builds credibility and trust with all stakeholders.

Step 4: Prioritize User Experience

Here a seamless user interface for both borrowers and investors is key to adoption. The platform should be fully responsive across devices and provide streamlined onboarding.

Step 5: Execute Development & Integration

Now you need agile development methodologies to build the platform. Moreover, you can also integrate reliable third-party services such as payment processors and identity verification systems. After that, rigorous testing for performance and usability at each stage is essential for operational excellence.

Step 6: Launch with an Ongoing Improvement Strategy

After deployment, establish mechanisms for continuous monitoring and user feedback collection. Consult with a banking app development company to stay adaptive to technological advancements based on your client’s needs.

Following this structured approach, you can capitalize on the advantages that well-developed P2P investment platforms offer.

Learn More,

The Future of Finance: Key Tech Trends Reshaping Banking

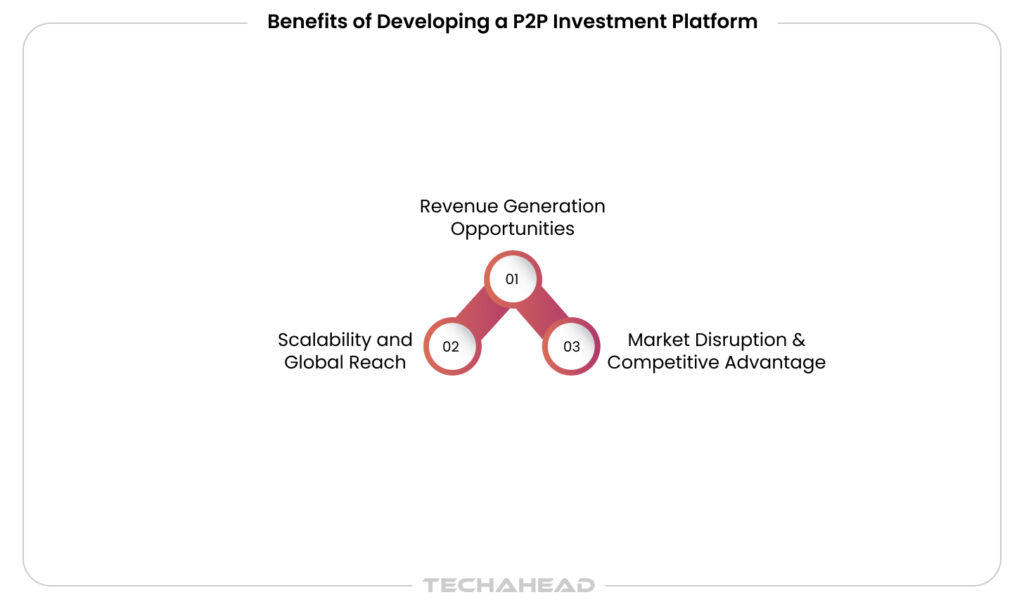

Benefits of Developing a P2P Investment Platform

Smart P2P platforms make money by being faster and easier than banks. P2P platforms have originated over $300 billion in loans globally, with top platforms generating 15-20% annual returns for investors while traditional banks struggle with 2-3% savings rates. Here are the other advantages that you can expect from investing in a P2P lending platform:

Revenue Generation Opportunities

When you develop a P2P investment platform, you are essentially creating multiple revenue streams that can ‘scale exponentially’. You can earn through origination fees (1-5% of loan amounts), servicing fees from ongoing loan management.

The beauty of this model is that once your platform gains traction, these fees compound as your loan volume grows.

Industry leaders like LendingClub have generated over $70 billion in loans that translate to hundreds of millions in platform fees. You are not just building a business, you are building a financial ecosystem that generates recurring revenue.

Market Disruption & Competitive Advantage

You have the opportunity to challenge traditional banking with better speed, transparency, and rates for both sides of the equation. While banks are burdened with legacy systems or say, regulatory overhead, your AI-powered P2P investment platform can approve loans in minutes rather than weeks. You can develop your own platform to position yourself in the $1 trillion alternative lending market.

Scalability and Global Reach

Generally, traditional lending institutions require physical branches, but your P2P platform scales globally with minimal infrastructure investment. You can hire cloud engineers to utilize technologies like cloud based architecture that gives you an opportunity to expand in new markets overnight. This lean operational model, combined with automated processes and AI-driven decision making, allows you to achieve better profit margins than traditional banks.

However, building a successful P2P platform is not easy; you need to understand key challenges that help you avoid costly mistakes.

Challenges of Building P2P Investment Platforms

Despite the massive profit potential, 40% of P2P platforms fail within their first three years mainly, due to regulatory issues and risk management failures. Here is how to navigate the most critical challenges:

Navigating Regulatory Compliance

The first major challenge is often changing regulatory environments and country specific compliance. Besides that, consider other requirements such as customer identity verification (KYC), anti-money laundering (AML) rules, data protection and many others.

Handing all these manually is simply impossible when it comes to building a leading P2P investment platform. That is why you must integrate automated regulatory compliance features to avoid penalties.

Managing Credit Risk and Defaults

Another challenge is accurately evaluating borrower creditworthiness and managing the risk of loan defaults. Many borrowers may lack traditional credit histories, so tough to assess their ability to repay. Higher default rates may lead to significant financial losses.

As a solution, you can consider advanced AI models that now analyze alternative data sources like social media behavior, transaction patterns, and mobile usage to assess creditworthiness with 85% accuracy for thin-file borrowers.

Preventing Cyberattacks

P2P platforms are frequent targets for fraud and cyberattacks. So protecting sensitive customer data and verifying borrower identities are essential to maintaining platform integrity. For this, you can rely on predictive analytics and advanced cybersecurity measures for carefully detecting suspicious activity early.

Learn More,

Real-Time Fraud Detection at Scale: Leveraging MLOps for Financial Services

Maintaining Liquidity in the Market

Another business challenge is maintaining liquidity; it means you need to have sufficient funds from investors ready to be lent. Economic downturns and changing market conditions limit liquidity and slow down lending activity.

Another aspect is that the markets already have many competing platforms, so making differentiation through innovation and superior customer service has become the most important aspect of this business.

Building User Trust

Finally, you need to gain the trust of both lenders and borrowers. Here the crucial aspects are the transparency of loan management, clear communication, and reliable performance tracking all contribute to building confidence in the platform.

Indeed, you can utilize the latest tech trends and add more features to address these challenges, as well as unlock new opportunities for competitive advantages.

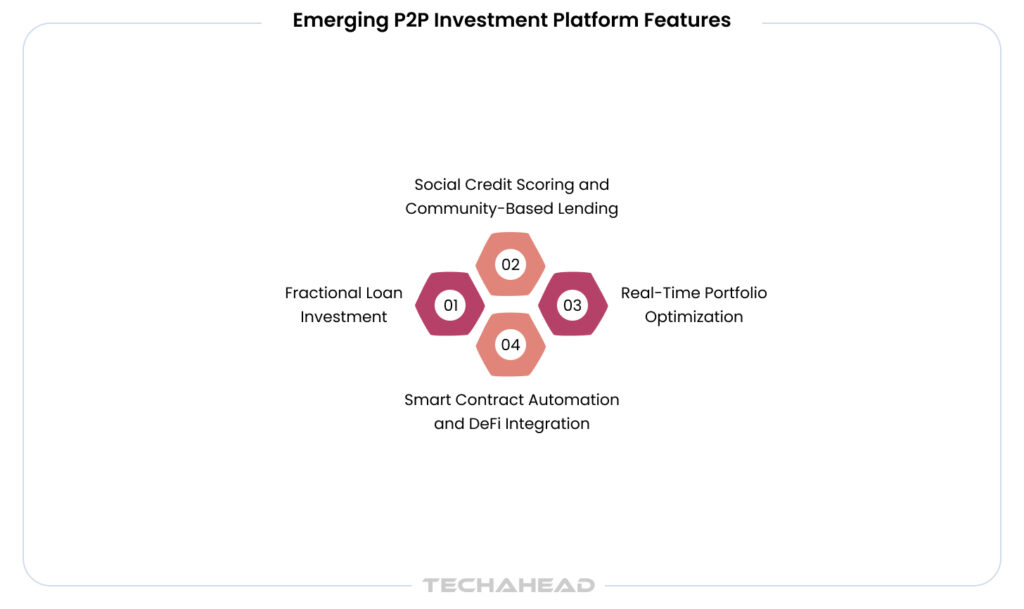

Emerging P2P Investment Platform Features

The most successful platforms are integrating next-generation features that turn the biggest P2P challenges into competitive advantages and build the trust that traditional platforms struggle to achieve.

Smart Contract Automation and DeFi Integration

The latest P2P platforms are revolutionizing loan management through blockchain-based smart contracts. You can consult with blockchain development companies to create self-executing contracts handle everything from loan disbursement to repayment collection; it means a reduction of operational costs by up to 60%.

When you integrate DeFi protocols, your platform taps into global liquidity pools. Platforms like MakerDAO have already proved how smart contracts manage billions in loans with minimal human intervention. You can expect better transparency and trust from such platforms.

Moreover, Aave’s automated lending protocol processes over $10 billion in transactions monthly. It shows how smart contracts eliminate intermediaries and maintain security.

Social Credit Scoring and Community-Based Lending

In the next few years, you will witness the emergence of social credit systems that evaluate borrowers based on community endorsements and social network analysis. These features allow creditworthy individuals with thin traditional credit files to access funding through social proof mechanisms.

You can integrate features like ‘peer vouching’, where community members stake their reputation on borrowers, and social collateral systems where borrowers’ social networks become part of the underwriting process.

This approach has shown remarkable success in emerging markets, with default rates dropping 40% when social validation is integrated into the lending decision.

For example, Kiva’s community-based microfinance model has provided over $1.6 billion in loans with 96% repayment rates through peer endorsements.

Real-Time Portfolio Optimization

Advanced P2P platforms now offer AI-powered robo-advisors for optimized loan portfolios based on different factors like market conditions, borrower performance, risk preferences. These systems use machine learning algorithms to automatically diversify investments across loan grades, terms, and geographic regions.

Real-time portfolio rebalancing reports 25% improvement in risk-adjusted returns through automated optimization. For instance, LendingClub’s automated investing feature manages $2 billion in investor portfolios that rebalance positions instantly based on market conditions.

Fractional Loan Investment

Modern platforms allow you to invest as little as $25 across hundreds of loan fragments. Prosper, for example, diversifies across 40,000+ loan fragments. This fractional investment approach spreads risk across thousands of micro-positions and maintains liquidity through secondary markets. You can now build a diversified P2P portfolio with minimal capital and access institutional-grade risk management tools.

Conclusion

The advanced technologies like artificial intelligence, machine learning, blockchain are reshaping finance. With some platforms processing over $300 billion globally and delivering 15-20% returns, the opportunity is huge. Smart contracts reduce costs by 60%, while AI-driven analytics cut default rates by 40%. Indeed, building a successful platform demands deep fintech expertise, regulatory knowledge, and technical excellence.

Are you ready to build your P2P investment platform? TechAhead is the leading fintech app development company that has delivered more than 100 successful financial applications. Contact us today to transform your P2P vision into a market-leading app that generates sustainable returns for years to come.

What is the development timeline for a full-featured P2P platform?

A P2P investment platform needs 8-12 months for development, including AI credit scoring, regulatory compliance integration, security testing, and user interface optimization. MVP versions can launch in 3-4 months.

How do P2P platforms generate returns of 15-20% for investors?

P2P platforms generate high returns by eliminating banking intermediaries, using AI-driven risk assessment to minimize defaults, charging borrowers competitive rates, and passing 80-90% of interest payments directly to investors.

How secure are P2P investment platforms against cyber threats?

Modern P2P platforms use bank-grade encryption, multi-factor authentication, blockchain technology, and AI-powered fraud detection, achieving 99.5% threat prevention. Regular security audits and regulatory compliance ensure investor protection.

What should investors look for when choosing a P2P platform?

Investors should prioritize platforms with transparent fee structures, strong regulatory compliance, proven track records, diversified loan portfolios, automated risk management, secondary market liquidity.

Which fintech development company offers the best P2P investment platform solutions?

TechAhead leads P2P platform development with 100+ successful fintech applications, specializing in AI-powered credit scoring, blockchain integration, regulatory compliance, and end-to-end solutions delivering proven ROI for clients globally.